May 10, 2026

Does My Employer Offer Daily Pay? How to Check

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

Two coworkers at the same warehouse both need $100 before Friday. Same shortfall, same week, same amount. Devon opens the earned wage access benefit his employer built into payroll and moves the money over. Across the break room, Tanya downloads a cash advance app she saw in an ad, links her checking account, and pulls the same $100. Both got their hundred bucks early. The question this article answers is the only one that matters over a year of doing this regularly: which path actually costs less, and who's really paying for it?

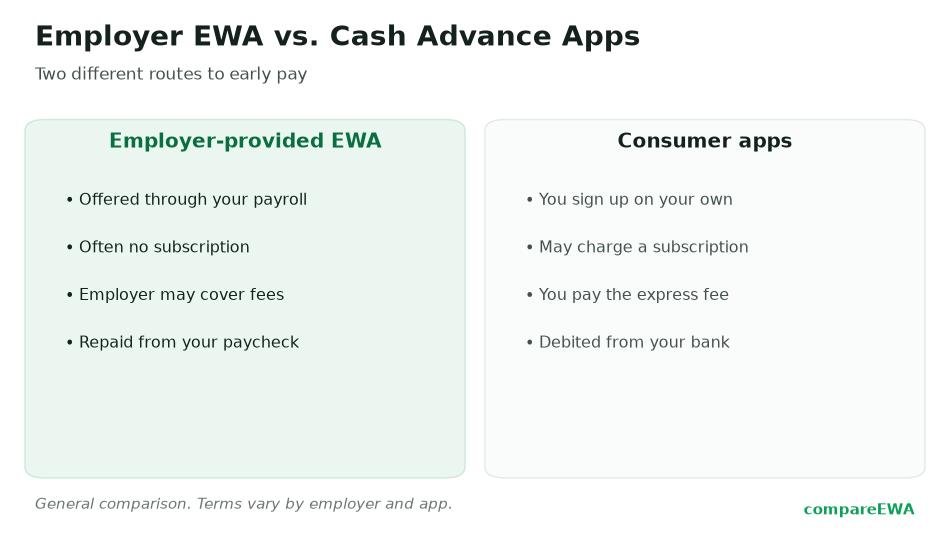

This is a comparison of two genuinely different products. One is employer-provided or payroll-integrated earned wage access (EWA), the kind offered through your job. The other is a consumer cash advance app you sign up for yourself. I'll keep them clearly separated, because the whole point is that they are not the same thing wearing different logos.

Start with the federal line that got drawn recently, because it maps almost perfectly onto the cost difference. A CFPB advisory opinion issued December 23, 2025 reaffirmed that qualifying employer-partnered earned wage access, meaning access only to already-earned wages, with no recourse against the worker and no underwriting, is not credit under the Truth in Lending Act. That advisory opinion superseded an earlier 2024 proposal that would have treated advances more like loans.

Why does a regulatory definition matter to your wallet? Because the same features that keep the employer model out of the "credit" bucket, no interest, no real risk to the lender, are the features that let it stay cheap. Many consumer apps, by contrast, lean on tips and express fees that behave like high-cost credit even when they avoid the word "loan." The official distinction and the cost distinction are basically the same line.

Employer/payroll-integrated EWA plugs into your employer's payroll and time-tracking system. It knows your verified hours, and when you take an advance, repayment is reconciled automatically out of your next paycheck. You're not writing a check back to anyone; the payroll run just nets it out.

Consumer apps work from the outside. You connect the app to your bank account, it estimates your earnings from your deposit history, and on payday it pulls repayment from that linked account by debit. It never sees your employer or your real hours. It's guessing, and it's collecting from your bank on its own schedule.

That structural gap, plugged into payroll versus plugged into your checking account, drives everything that follows about cost and risk.

The CFPB's July 2024 Data Spotlight on the paycheck advance market put hard 2022 figures on both models, and the contrast is stark. Label these as 2022 usage data; the market has grown since, but the shape of the difference holds.

On the employer-partnered side: about $22.8 billion was advanced across 214 million transactions, used by 7.2 million workers, with an average transaction of $106.73. Roughly 90 percent of workers paid at least one fee, but the average fee per transaction when charged was $3.18, and average annual fees per worker came to $68.88. Almost all of that, 96.61 percent, was expedited-transfer fees, meaning the money workers paid was mostly for choosing instant delivery over the free slower option.

On the direct-to-consumer side: about $9.1 billion was advanced to roughly 3 million consumers, and 73 percent of transactions included a tip averaging $4.09. The CFPB's illustrative figure for a $144 seven-day advance worked out to an APR of about 290 percent. Other research points the same direction. The Center for Responsible Lending, an advocacy group whose stance leans hard against these products, reported average APRs near 383 percent on app advances repaid in 7 to 14 days. Those two APR figures come from different samples and methods, so don't treat them as directly comparable, but both land in payday-loan territory.

Set the annual numbers side by side. Under $70 a year in mostly optional speed fees on the employer side. Tips plus express charges that compound into triple-digit effective APRs on the consumer side. For the same $100.

Follow the money and the reason for the gap becomes obvious. Employer programs are typically offered at no cost to the company, or close to it, and they usually include a free transfer option that just takes one to three days to land. You pay only if you want the money instantly. So on the employer side, the company is absorbing the cost of the plumbing, and you're paying at most a small expedite fee you can often skip by planning a day ahead.

Consumer apps have no employer footing the bill. Their entire revenue comes from you, through express fees and "optional" tips. And that word optional deserves the scare quotes. As plenty of workers have figured out, skipping the tip can quietly shrink the limit you're offered next time, so the tip isn't as voluntary as it looks. When the product has to earn its money from the worker, the worker pays more. It can't work any other way.

If you want one number that explains why the consumer model has to charge so much, it's the charge-off rate, the share of advances that never get repaid. In the CFPB's 2022 data, employer-partnered programs charged off just 0.3 percent. Direct-to-consumer advances charged off 6.3 percent, more than twenty times higher.

That makes sense once you see the mechanics. The employer program gets repaid straight out of payroll, so it almost always collects. The consumer app is chasing repayment from a bank account it doesn't control, so far more of its advances go bad, and it has to price that risk into what everyone pays. High losses force high fees. The default gap and the fee gap are the same story told two ways.

For a sense of scale on the other side, a Harvard Kennedy School working paper by Baker and Kumar found that an employer-integrated advance of $200 cost roughly one-seventh of what a typical overdraft fee would run for the same shortfall. Used for a genuine gap, the employer version can be dramatically cheaper than the overdraft it replaces.

I don't want this to read like an ad for the employer model, because it has real limits and one real trap.

First, it's only available if your employer offers it. Plenty don't. Second, the free option is slow, one to three days, so in a true same-hour emergency you're either paying the small expedite fee or you're out of luck. Third, and this is the one that bites regardless of how cheap the access is: any early access borrows from the same paycheck. Lean on it every week and every paycheck shrinks, and you can slide into a cycle where you're always a little behind, even at a low fee. The Center for Responsible Lending documented that heavier users of consumer advance products saw checking-account overdrafts rise 56 percent, with heavy users paying about $421 in combined loan and overdraft fees in their first year. The employer model is far cheaper per use, but habitual use of any early-pay tool moves your shortfall forward rather than fixing it.

So the honest verdict: if your job offers earned wage access, it will almost certainly cost you less than a consumer app, often by an enormous margin, and it carries far less risk of a debt spiral. Use it for specific gaps and take the free slower transfer when you can. But cheaper access is still access to your own future paycheck, so the real win is needing it less over time, not using it more because it's cheap.

Usually the slower transfer (one to three days) is free to the worker, and you pay only if you want the money instantly. In the CFPB's 2022 data, average annual fees per worker on employer-partnered programs were $68.88, almost all of it optional expedited-transfer fees. It's low-cost, and much of the cost is avoidable if you plan a day ahead.

Tips are a main way consumer apps make money, since no employer is paying for the service. You can usually skip the tip, but many workers report that skipping it can lower the amount you're offered next time, so it functions less like a true tip than it appears.

Almost always. CFPB 2022 data showed employer-partnered advances carried small, capped fees averaging $3.18 per transaction when charged, while direct-to-consumer advances carried tips plus fees that translated into effective APRs around 290 percent. The employer version is typically far cheaper for the same amount.

No. A CFPB advisory opinion issued December 23, 2025 reaffirmed that qualifying employer-partnered earned wage access, with access only to already-earned wages, no recourse, and no underwriting, is not credit under the Truth in Lending Act.

Rarely on cost. The main reason would be availability of a specific feature or a faster option in a same-hour emergency, but you'll almost always pay more with a consumer app. If your job offers it, start there.

Two things. The free transfer is slower (one to three days), so instant delivery costs a small fee. And even cheap access is still an advance on your own paycheck, so using it every week shrinks each deposit and can quietly become a habit that keeps you a step behind.

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

How same-day and on-demand pay reshapes cash flow for workers used to a biweekly cycle, and the tradeoffs of pulling pay early.

Read article

How earned wage access works for hourly and shift workers with variable hours, and what you can safely pull before payday.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking