June 12, 2026

How Cash Advance Apps Work, Start to Finish

See exactly how cash advance apps work, from linking your bank to the payday auto-debit, so nothing about them feels mysterious.

Read article

The pitch you'll hear from almost every cash advance app is some version of "we're not a payday loan." It's a smart line, because payday lending has a deservedly rough reputation. But a marketing claim isn't a fact, so let's test it. When you put earned wage access and payday loans side by side and look at actual regulator data, how different are they really? The short answer: EWA is usually cheaper and less punishing per use, but the repeat-use pattern can start to look uncomfortably familiar.

Here's the honest comparison, with real numbers, so you can decide which one is genuinely less harmful for your situation, or whether to skip both.

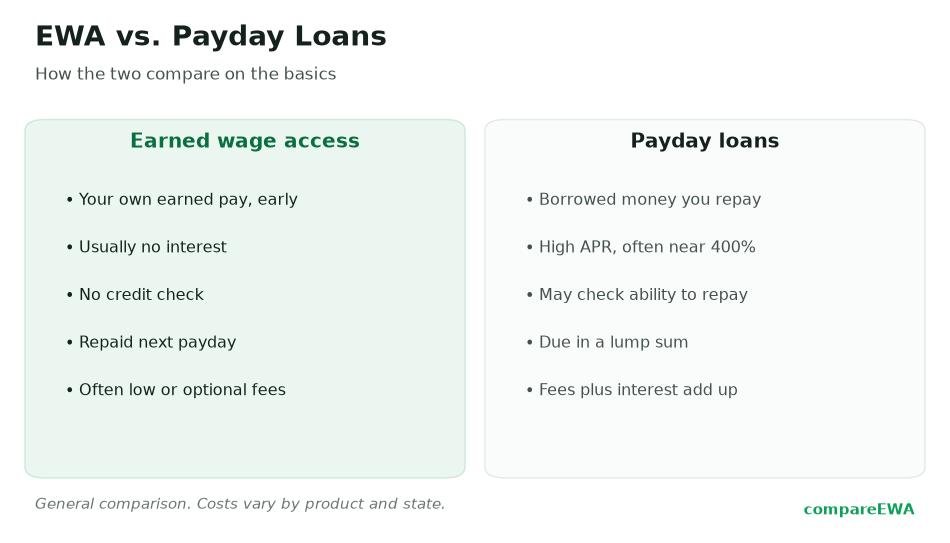

If you take one advance and repay it on time, earned wage access is almost always the cheaper, lower-risk option. It tends to cost a few dollars rather than a $15-per-$100 fee, and many EWA products won't sue you or report you to the credit bureaus. But if you use either product every single pay period, the gap narrows, because frequent EWA use stacks up small fees the same way a payday cycle stacks up big ones. Neither builds your credit. Both can become a habit. The details below break down why.

A payday loan is a small, short-term, high-cost loan, usually due on your next payday, and it is explicitly a loan with a finance charge. Nobody disputes that classification. You borrow money that isn't yours yet, and you pay a fee for it.

Earned wage access is framed differently: it's access to wages you've already earned but haven't been paid, repaid on payday, and marketed as "your own money, early." That framing is doing a lot of work, and whether it holds up legally is the fight I'll cover next. The CFPB's plain-language explainers on how APR works on short-term loans are a clean primary source if you want the official definitions.

If the "is EWA a loan?" question feels confusing, that's because regulators themselves have gone back and forth. The Consumer Financial Protection Bureau issued a 2020 advisory opinion suggesting some no-cost, employer-based EWA wasn't credit. In July 2024 it proposed an interpretive rule treating many EWA products as credit under the Truth in Lending Act. Then, on December 23, 2025, it reversed course again and reaffirmed that qualifying "Covered EWA" is not credit under TILA, rescinding the 2024 proposal.

Consumer advocates aren't convinced by the "not a loan" framing. The National Consumer Law Center argues that fee-charging EWA functions as a loan regardless of the label, a position it lays out in its analysis that earned wage payday loans are loans. So you've got a federal regulator that landed on "not credit," and advocates who say that misses how the product actually behaves. Both views are worth holding as you read the cost numbers, because how you classify EWA shapes which protections apply, a point our guide on whether cash advance apps are safe gets into.

This is the heart of it, and it's where both industries spin. Let me give you both lenses, because each tells a different truth.

On a per-use dollar basis, payday is clearly more expensive. A typical two-week payday loan with a $15 fee per $100 borrowed works out to roughly a 400% APR, and in some states it can climb past 600%. The Center for Responsible Lending's research on APRs on single-payment payday loans documents just how high those rates run.

Now here's the part EWA marketing leaves out. When you count all the fees, tips, and optional charges, EWA APRs are not automatically low. California's Department of Financial Protection and Innovation, analyzing 2021 data, found average APRs of about 334% for tip-based companies and 331% for non-tip companies once mandatory fees, tips, and optional fees were included. Those figures are in the DFPI's 2021 Earned Wage Access data findings. That's a contested methodology, and it's only fair to say so: the DFPI counted tips and optional fees that some providers argue are voluntary and shouldn't be treated as finance charges. Still, the numbers puncture the idea that EWA is automatically cheap on an APR basis.

A different federal dataset softens the picture for employer-partnered EWA. The CFPB's July 2024 paycheck advance data spotlight put an illustrative APR around 109.5% for that market, with an average transaction of about $106 and an average fee of $3.18 when a fee applied. Both things can be true at once: the per-transaction dollar cost is often low (a few dollars), while the APR looks high because the term is so short (about ten days). Here's how to hold both:

The cost advantage of EWA depends on using it rarely. The data says a lot of people don't. California's DFPI found consumers took an average of 36 advances per year, with some reaching around 100. The CFPB's employer-partnered data found an average of 27 transactions per year. Either way, this is not a once-in-a-blue-moon product for many users; it's a recurring one.

Payday has its own version of this. The CFPB has found that roughly 80% of payday loans are rolled over or reborrowed within two weeks, and a large share of borrowers take out ten or more loans a year. So both products have a repeat-use pattern baked in. The difference is that EWA is cheaper per use, which means frequent use erodes its advantage more gently, but it still erodes it. Thirty-six small fees a year is still thirty-six fees. If you find yourself reaching for an advance every pay period, the "it's only three bucks" logic stops holding, and the deeper problem, a paycheck that doesn't stretch, is the one worth solving.

Where EWA genuinely tends to pull ahead is what happens when things go wrong. The structures differ in ways that matter:

That patchwork is real and consequential. Nevada licenses EWA and builds in non-recourse protections, as our piece on the rankings and how we evaluate apps and the state-law coverage explain. Connecticut treats EWA as a small loan with hard fee caps, which our look at how Connecticut treats EWA like a loan covers, and Nevada's approach set the template many states copied, detailed in our piece on the Nevada earned wage access law. So the protections you actually get depend heavily on where you live.

If you need a small amount once, and you'll repay it on your next check without stacking another advance right after, earned wage access is usually the less harmful option in real dollars, and its non-recourse structure means a stumble won't wreck your credit or land you in court. Choose the no-cost option, skip the tip, and you may pay very little.

If you're reaching for an advance every pay period, though, neither product is your answer, they're both treating a symptom. And if a payday loan is your only option in a state that caps or bans them, that ban usually exists for a reason worth respecting. The genuinely useful move, when you can manage it, is putting even a small buffer between yourself and the next shortfall, so you're not paying a fee to reach your own paycheck a few days early, month after month.

Not legally, at least under the current federal view. As of December 2025 the CFPB treats qualifying EWA as not credit under the Truth in Lending Act, while a payday loan is explicitly a loan. Functionally, though, consumer advocates argue fee-charging EWA behaves like a short-term loan, and heavy repeat use of either can look similar.

For a single, occasional advance, EWA is usually cheaper in real dollars, often a few dollars versus a $15-per-$100 payday fee. But when all fees and tips are counted, EWA APRs can still be high (California's DFPI found averages around 331% to 334%), and frequent use erodes the savings.

Because APR annualizes a short-term cost. A $3 fee on a ten-day advance looks tiny in dollars, but stretched over a year it produces a large percentage. The CFPB illustrated an APR around 109.5% for the employer-partnered market even though the average fee was about $3.18.

Many EWA products are non-recourse and do not report nonpayment to credit bureaus, so they typically will not hurt your score. Payday lenders can, in some cases, pursue collection or report you. Neither product typically builds credit, either.

Generally no. Tips are usually optional, and several state laws require a zero-dollar tip option. Some apps present tips in a way that makes them feel mandatory, so look for the no-tip choice before confirming a transaction.

It varies by state. Because EWA is often regulated differently from payday lending, it can be available in some states with strict payday rules, but not always. Connecticut, for example, folds EWA into its Small Loan Act, while other states license it separately. Check your state's specific rules.

See exactly how cash advance apps work, from linking your bank to the payday auto-debit, so nothing about them feels mysterious.

Read article

Are cash advance apps safe? What they can see when you link your bank, the protections you have, and the gaps that remain.

Read article

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking