May 21, 2026

New York Earned Wage Access Law: The Rules Now

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

When people ask me which state law to understand first if they want to grasp how earned wage access is regulated in America, my answer is Nevada. The Nevada earned wage access law was the first of its kind in the country, and it did something the others hadn't: it built a full licensing system, wrote in real consumer protections, and set a pattern that state after state has since borrowed. If you use these apps anywhere, understanding Nevada's rules tells you what "good" regulation of this product looks like.

Let me walk through what Nevada built, who enforces it, and the protections a Nevada user actually gets, then explain why so many other states copied it.

Earned wage access apps are legal in Nevada, and they're legal in a specific, deliberate way: providers must hold a state license to operate. That's the notable part. Nevada didn't just tolerate these apps, it created a licensing regime for them and put a state regulator in charge. Being legal in Nevada means being licensed in Nevada.

That's a stronger footing than the situation in a state with no EWA law at all, where the apps run legally but with no dedicated oversight. In Nevada, the license itself is the front door, and a provider that hasn't walked through it isn't supposed to be serving Nevada residents.

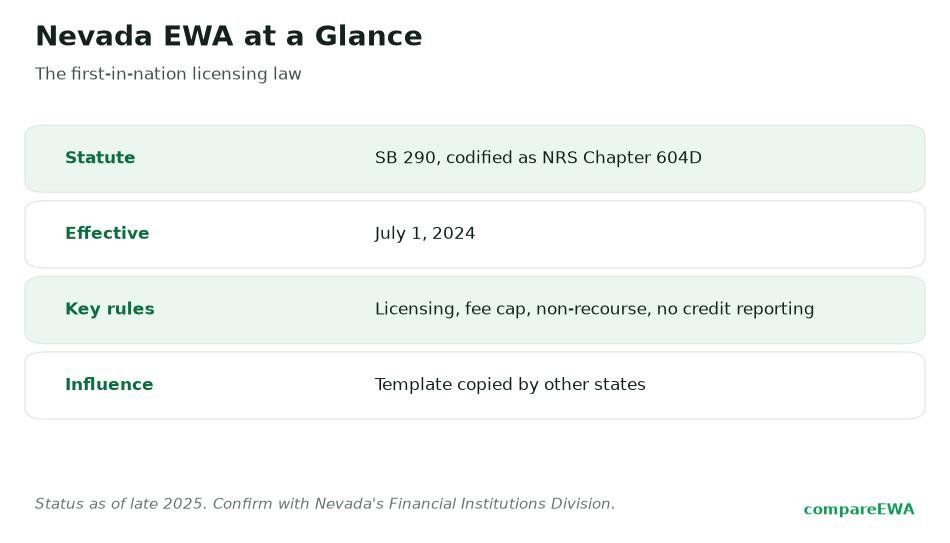

The law is Senate Bill 290, signed by Governor Joe Lombardo on June 15, 2023. It was the first state law in the nation to license earned wage access providers, and it's codified as Chapter 604D of the Nevada Revised Statutes, titled Earned Wage Access Services. You can read the codified chapter on the Nevada Legislature's NRS 604D page.

SB 290 covers both flavors of the product: "employer-integrated" services, where the app works through your employer's payroll, and "direct-to-consumer" services, where you connect the app to your own bank account without your employer's involvement. That breadth matters, because a lot of the apps people actually use are direct-to-consumer, and some state proposals elsewhere only reach the employer-linked kind.

The statute also settles the classification question in a way that favors clarity. Under Nevada law, EWA services provided by a licensee do not constitute loans, credit, or money transmission. Licensees are not deemed creditors, lenders, or money transmitters, and their fees are not treated as interest or finance charges. In other words, Nevada looked at the product and decided to regulate it as its own thing rather than force it into lending law. That's the opposite of the approach Connecticut took, which routed these advances through its existing small-loan lending law instead.

The regulator is the Commissioner of Financial Institutions, working through the Nevada Financial Institutions Division, or FID. A provider has to obtain a license from the FID before it can operate, and the application isn't a rubber stamp. It requires:

Nevada capped the application and license fees (both initial and renewal) at $1,000, so the cost of entry is meaningful but not prohibitive. The FID maintains the list of licensed providers, and you can verify a company through the Nevada Financial Institutions Division. If you want the statutory text corroborated from a second source, the chapter is also published at Justia's copy of Nevada Chapter 604D.

This is where Nevada earns its "template" reputation. SB 290 doesn't just register companies, it writes concrete protections into the relationship. A Nevada user of a licensed provider is entitled to the following:

Read that list again, because each item answers a fear people actually have. Worried an unpaid advance could wreck your credit? Nevada bars credit reporting on it. Worried the app's auto-debit could overdraw you and stick you with a bank fee? Nevada makes the provider pay that back if the provider caused it. Worried you'll get stuck in a product you want out of? You can cancel any time for free. These are the protections a lot of users assume they have everywhere. In Nevada, they're written into the statute.

Nevada didn't cap fees outright, but it did put guardrails around the pieces that trip people up. On tips, providers have to give you the option to choose a zero-dollar gratuity and follow disclosure requirements around how tips are presented. That's aimed squarely at the "I thought the tip was mandatory" problem that has dogged this industry.

On access, the mandatory no-cost option is the quiet hero of the law. It means a Nevada user always has at least one free path to their earned wages, even if the instant-transfer option carries a fee. You might still choose to pay for speed, but you're never forced to pay to get your own money at all. That single requirement does a lot of protective work, and it's one of the features other states copied most faithfully.

Still, "no-cost option available" doesn't mean the app you pick is the cheapest one for how you actually use it. Comparing express fees and any subscription costs across providers is worth the few minutes, and our EWA app rankings line those up. Our review of the top-rated pick, Cashzella, breaks down its specific costs.

Nevada moved first, and it moved with a model that was easy for other legislatures to adapt: license the providers, require a no-cost option, put rules around tips, and make repayment strictly non-recourse. Because it was coherent and consumer-facing, it became the blueprint. Missouri passed its own version in 2023, Wisconsin followed in March 2024, Kansas in April 2024, and South Carolina joined the list, with more states enacting or weighing similar laws through 2025 and into 2026. The National Conference of State Legislatures keeps a current tracker of state EWA legislation if you want to see the full and growing map.

The lesson for a reader is simple: when you see a state EWA law with a licensing requirement, a free option, tip disclosures, and non-recourse repayment, you're usually looking at Nevada's DNA. Understanding NRS 604D is a shortcut to understanding a dozen other state laws at once. Not every state followed the template, though. California regulated the product but declined to cap fees or require the same protections, as our piece on the California earned wage access law explains.

Nevada's timing looks even smarter in hindsight. On December 23, 2025, the Consumer Financial Protection Bureau reaffirmed that qualifying earned wage access is not credit under the federal Truth in Lending Act, and it rescinded a July 2024 proposal that would have treated many of these products as credit. With the federal government stepping back from regulating EWA as lending, state licensing regimes like Nevada's became the primary consumer safeguard rather than a supplement to federal rules.

That's the "states are leading" story in one sentence: the safeguards that matter most for these products now live in state law, and Nevada wrote the first serious version of it. If you live in a Nevada-style state, you're covered by real protections. If you live in a state with no EWA law, the federal retreat leaves a thinner net, which is why knowing your own state's status genuinely matters. Before you connect any app, it's also worth understanding whether cash advance apps are safe and what they can see once linked, and if you're weighing an advance against a payday loan, our earned wage access versus payday loans comparison runs the real cost math.

A note on precision: the exact section numbers within NRS 604D can shift as the code is amended, so if you need to cite a specific subsection, confirm it against the Nevada Legislature's current text. The structure and protections described here are the core of what SB 290 created.

Yes. Earned wage access apps are legal in Nevada, but providers must hold a license from the Nevada Financial Institutions Division to operate. Being legal in Nevada means being licensed there.

Yes. Nevada's SB 290, signed on June 15, 2023, was the first state law in the nation to license EWA providers. It is codified as NRS Chapter 604D.

SB 290 is the 2023 law that created Nevada's EWA licensing regime, now codified as NRS Chapter 604D. It requires providers to be licensed, covers both employer-integrated and direct-to-consumer services, states that licensed EWA is not a loan or credit, and builds in consumer protections like a no-cost option and non-recourse repayment.

Yes. Under NRS 604D, licensed providers must offer at least one no-cost way to access your earned wages. You may choose to pay for faster delivery, but you cannot be required to pay anything to get your own money.

No. Nevada's law bars licensed providers from reporting delinquencies to credit agencies, pursuing civil collection actions, using third-party debt collectors, or selling the debt. Advances are non-recourse.

Several. Missouri (2023), Wisconsin (March 2024), Kansas (April 2024), and South Carolina enacted similar licensing frameworks, with more states following through 2025 and 2026. Nevada's model of licensing plus a no-cost option and non-recourse terms became the widely copied template.

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

Is earned wage access legal in Texas? How the state treats these apps, the bills that failed, and what it means for users.

Read article

How California's DFPI treats earned wage access, what registration means, and what the rules change for you as a borrower.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking