May 21, 2026

New York Earned Wage Access Law: The Rules Now

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

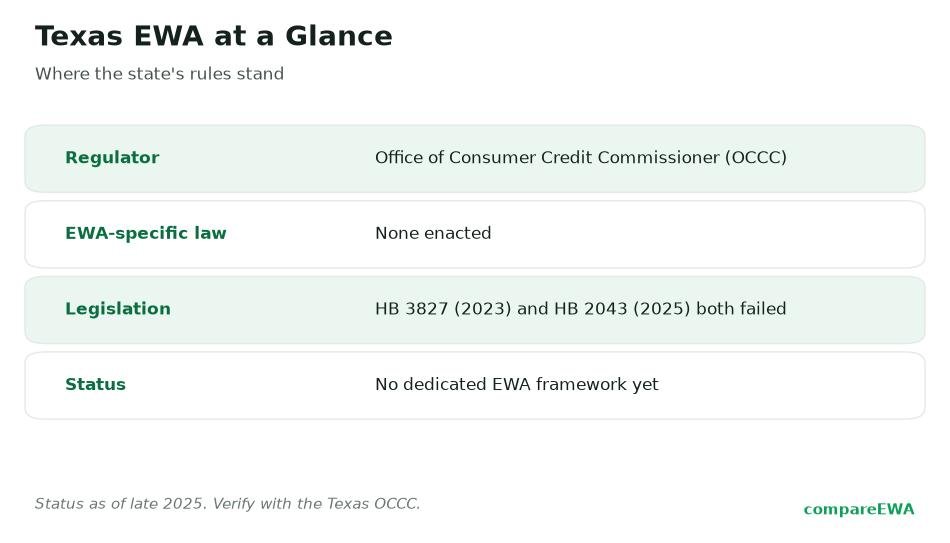

The Texas earned wage access law is unusual for a reason most people wouldn't guess: there isn't one. Texas is a huge state where cash advance apps are common and completely legal, yet lawmakers have tried twice to pass a dedicated framework for them and both attempts failed. That leaves a real question for anyone in Texas about to link a bank account to one of these apps: if there's no EWA-specific law here, who's watching the companies, and what are you actually protected from?

Let me answer the legality question up front, then explain the gap and what it means for you day to day.

Yes, they're legal. Earned wage access apps operate freely across Texas today. What's missing isn't permission, it's a rulebook written specifically for them. Texas has no statute that licenses EWA providers, caps their fees, or sets conduct standards tailored to the product.

That's a different situation from a state like Nevada or California, where lawmakers built dedicated EWA rules. In Texas, the apps run legally but outside any bespoke guardrails. Legal and regulated are not the same thing, and in Texas the product is the former without much of the latter.

This isn't for lack of trying. The Texas Legislature has taken up EWA twice in recent sessions, and each bill died before becoming law.

The first attempt came in 2023. The second came in 2025, moved further through the process, and then stalled on a procedural point. Neither is on the books. I'll walk through what each one would have done, because the details tell you a lot about the fight that's still unresolved.

One important framing before the specifics: a bill passing one chamber is not the same as a bill becoming law. Texas coverage sometimes blurs that line. Both of these measures cleared hurdles that made headlines, and both still failed to reach the governor's desk.

HB 3827, filed in the 88th Legislature in 2023, would have created an occupational license for EWA providers, defined the product as explicitly not a loan, and exempted it from the usury and rate-and-fee limits that apply to Texas credit. The Texas House passed it on May 5, 2023, by a vote of 91 to 52. Then it stalled in the Senate and died before the session ended. Passed one chamber, never became law.

HB 2043, filed in the 89th Legislature in 2025 by Representative Lambert (with a companion, SB 938, from Senator Parker), took a somewhat different tack. It would have added a new Chapter 398 to the Texas Finance Code to regulate EWA providers and give the state authority to impose administrative penalties. It was reported favorably, as substituted, out of the House Committee on Pensions, Investments and Financial Services on March 31, 2025. But on April 29, 2025, a point of order was sustained against it, sending it back to the Calendars Committee, where it stalled. The regular session adjourned sine die on June 2, 2025, so HB 2043 never became law either. You can follow the full record on the Texas Legislature's official bill history for HB 2043.

The two bills also drew a predictable split. The Financial Technology Association supported HB 2043 as providing "clarity" for the industry. Consumer advocates at Texas Appleseed opposed both bills, arguing they'd let wage-advance products, in the group's words, "evade consumer protections" and operate as a new form of high-cost lending. Those are competing positions, not settled facts, but they frame the stakes: one side wanted a light-touch license, the other worried a weak law would be worse than none. You can read the advocacy case on the Texas Appleseed site.

Here's a contrast that surprises people. Texas regulates payday and auto-title lending heavily. It barely regulates EWA at all.

Texas payday and auto-title lenders operate as Credit Access Businesses under Chapter 393 of the Finance Code, and the underlying loans fall under Chapter 342. The state is well known for high payday costs, but the point is that a whole licensing and disclosure structure exists around that product. EWA apps sit entirely outside that regime. They aren't Credit Access Businesses, and they aren't covered by those chapters.

That's exactly the disconnect consumer advocates worry about. Because EWA apps live outside the payday framework, they can charge express-transfer fees and solicit tips without the caps that apply to regulated credit. Whether that's a fair deal depends heavily on how often you use the app and how much you pay per advance. Our comparison of earned wage access versus payday loans runs the actual numbers, and they're not as one-sided as either industry likes to claim.

With no EWA-specific law, the answer is a patchwork rather than a single agency. The Texas Office of Consumer Credit Commissioner (the OCCC) administers the state's consumer-credit statutes and would have been the natural home for EWA oversight if HB 2043 had passed. It didn't, so the OCCC doesn't license these apps. You can still learn what it does regulate at the OCCC's official site.

Federal law doesn't fill the gap for direct-to-consumer apps either. On December 23, 2025, the Consumer Financial Protection Bureau reaffirmed that qualifying, employer-partnered "Covered EWA" is not credit under the federal Truth in Lending Act, and it rescinded a July 2024 proposal that would have treated many EWA products as credit. The practical effect for Texas: the federal disclosures that would standardize an advance's cost generally don't attach, and there's no state EWA law behind them, so much of the protective load falls on you and on general consumer-protection tools.

That doesn't leave you with nothing. Standard protections still apply to your bank account, like your dispute rights over unauthorized electronic transfers. But those are backstops, not EWA-specific rules. If an app takes money you didn't authorize, that's a different problem from an app charging a steep-but-disclosed instant-transfer fee, and only the first has a clear legal remedy.

Because there's no state cap or mandated disclosure, the burden of reading the fine print sits with you. A few things I'd check before linking an account in Texas:

Understanding what an app can see and pull once it's connected is its own topic, and worth reading before you tap "link account." Our guide to whether cash advance apps are safe covers the data side. And because fees vary so much between apps with no Texas cap to level them, comparing options directly matters more here than in a capped state. Our EWA app rankings put the fee structures side by side.

It's also worth knowing how other states handled the same product, since Texas may revisit this. California built a registration system with a non-recourse promise; our piece on the California earned wage access law explains it. Nevada went further still, and the Nevada earned wage access law became the template several states copied. Texas could pick up the thread in a future session, so treat "no law" as the current status, not a permanent one.

Yes. Earned wage access apps are legal and widely used across Texas. There is simply no state statute written specifically for them, so they operate without a dedicated licensing or fee framework.

Not with an EWA-specific law. Two bills that would have created one, HB 3827 in 2023 and HB 2043 in 2025, both failed. The Office of Consumer Credit Commissioner administers Texas consumer-credit statutes but does not currently license EWA providers.

No. Texas payday and auto-title lenders are heavily regulated as Credit Access Businesses under the Finance Code. EWA apps sit outside that regime entirely, which is both why they avoid payday-style caps and why advocates worry they escape consumer protections.

HB 2043 was reported favorably out of a House committee on March 31, 2025, but a point of order was sustained against it on April 29, 2025, returning it to the Calendars Committee, where it stalled. The regular session adjourned on June 2, 2025, so it did not become law.

No. With no EWA-specific statute, there is no state cap on express-transfer fees, tips, or subscription charges for these apps in Texas. Two legal apps can charge very different amounts for the same advance.

There is no single EWA regulator in Texas. For general consumer-credit concerns the Office of Consumer Credit Commissioner is a starting point, and unauthorized transfers from your bank account fall under federal electronic-transfer protections you can raise with your bank and the CFPB.

Where New York's earned wage access rules stand, the competing bills in play, and what an unsettled law means for users.

Read article

How Nevada's first-in-nation earned wage access law works and why other states copied its licensing template.

Read article

How California's DFPI treats earned wage access, what registration means, and what the rules change for you as a borrower.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking