June 12, 2026

How Cash Advance Apps Work, Start to Finish

See exactly how cash advance apps work, from linking your bank to the payday auto-debit, so nothing about them feels mysterious.

Read article

The moment that makes most people hesitate with a cash advance app is the one where it asks to connect to your bank account. That hesitation is healthy. But it's often pointed at the wrong risk. When people ask whether cash advance apps are safe, they usually picture an app draining their checking account or a hacker stealing their login. Those aren't the failures that actually happen most. The real risks are quieter, and they're mostly about fees and consent, not theft.

So let me give you the honest, unsentimental version: what an app can see once you link your bank, how that connection technically works, which consumer protections cover you and which don't, and a concrete checklist to lower your risk before you tap "connect."

For most users, the thing that goes wrong isn't a stolen account. It's a charge they didn't fully understand: an instant-transfer fee that made a "free" advance cost real money, a "tip" that felt mandatory, or a monthly membership quietly debited long after they stopped using the app. Those are consent and disclosure problems, and they're common enough that a federal regulator built an enforcement case around them.

That reframing matters because it changes how you protect yourself. Guarding against hacking is mostly about the app's security. Guarding against surprise fees is about reading the screens carefully and knowing your rights. The second is where your attention is better spent.

There are two main ways an app connects to your bank, and the difference affects your risk.

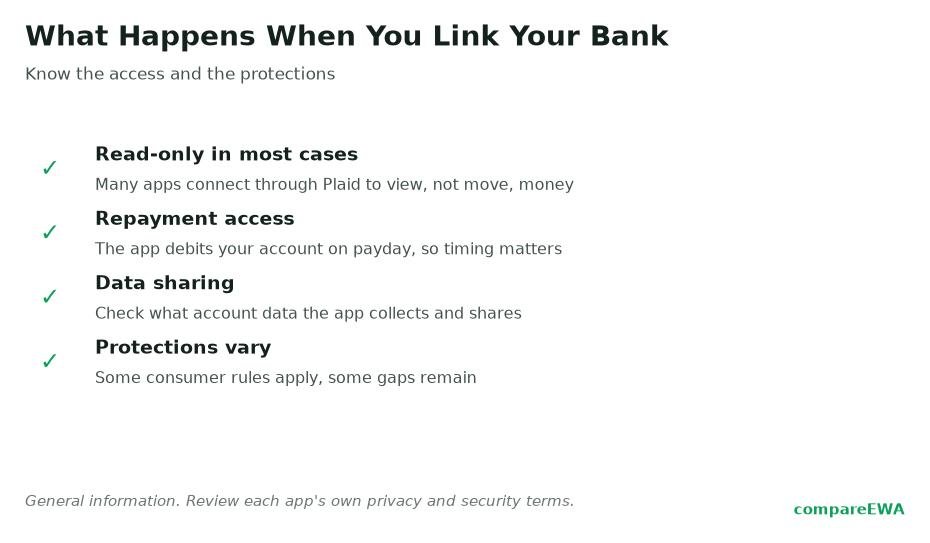

The more common and generally safer method uses a data aggregator, a middleman service like Plaid, MX, or Finicity. You authenticate at your own bank's login screen, and the app receives a token plus read access to your account data. Crucially, in a token-based connection the app doesn't hold your actual bank password; it holds a permission token that can be revoked. Plaid's own earned wage access overview describes how that connection works, though keep in mind it's the vendor's perspective.

The other method is direct login, sometimes called screen scraping. Here you may hand the app your actual bank username and password, and the app logs in as if it were you. That's riskier, because you've shared reusable credentials rather than a revocable token. If an app offers a choice, a token-based connection is the safer default. If it insists on your raw bank password, that's a reason to slow down.

Once connected, a cash advance app typically sees more than the balance. Read access to a checking account usually reveals:

Here's the part worth sitting with: apps use this data to make underwriting-like decisions, judging how much to advance you and when to pull repayment, even when the product carefully avoids calling itself credit. So you're being assessed on your account patterns whether or not the app uses the word "loan." That's not sinister on its own, but you should know your spending and income data is doing work behind the scenes, and that the aggregator may retain and share some of it. Aggregators have faced privacy litigation over how they collect and share data, so it's fair to check what an app and its aggregator keep, and whether you can revoke access later.

If you want a concrete picture of what "unsafe" looks like in practice, look at the federal action against Dave, a major cash advance app. In November 2024 the Federal Trade Commission brought a case against Dave, and in December 2024 it referred the matter to the Department of Justice. Note the framing carefully: these are allegations, and the case was referred rather than finally decided, so nothing here is a proven verdict. You can read the FTC's own account in its press release on the Dave action, with additional detail in Banking Dive's coverage.

According to the FTC's allegations, the problems weren't hacking. They were fees and consent:

Whatever the case's final outcome, the pattern it describes is the exact risk profile to watch for: costs that hide inside speed, tips, and subscriptions, and consent that's easy to give by accident. That's what unsafe usually means with these apps, and it's why comparing fee structures before you commit is worth the effort. Our EWA app rankings lay those costs out, and our review of the top-rated option, Cashzella, itemizes its fees.

Now the rights side, because it's genuinely mixed. Some protections are solid, one important one may not apply.

The Electronic Fund Transfer Act, and its Regulation E, covers unauthorized electronic transfers from your account and gives you error-resolution and dispute rights. If money leaves your account without your authorization, this is your practical backstop, and it's a real one. The FTC Act, which bars unfair or deceptive practices, is the other backstop, and it's exactly what the FTC used against Dave.

The gap is the Truth in Lending Act, or TILA. Whether TILA applies to these products is contested, and as of December 23, 2025, the Consumer Financial Protection Bureau's position is that qualifying "Covered EWA" products are not credit under TILA. That matters because TILA is the law that would normally force standardized cost disclosures. If it doesn't attach, the very disclosures that would spell out an advance's true cost may not be federally required. Coverage of that position is in the ABA Banking Journal. Treat it as the current federal stance, which could shift, and don't assume an app is "regulated like a bank," because it generally is not; oversight varies by state and by product, as our comparison of earned wage access versus payday loans and our look at how Connecticut treats EWA like a loan both show.

Before you link a bank account, run through these:

Leaving cleanly is part of safety. If you decide an app isn't for you, do more than delete it from your phone, because deleting the app doesn't cancel a subscription or revoke bank access. Cancel any membership inside the app first, then revoke the app's connection. If you connected through Plaid or a similar aggregator, you can typically manage or disconnect linked apps through the aggregator's portal as well as through your bank's connected-apps settings.

If something already went wrong, use the formal channels. Unauthorized transfers are a Regulation E matter you can raise with your bank. Deceptive fee or tip practices can be reported to the FTC at reportfraud.ftc.gov, and you can file a complaint about a financial product with the CFPB through its consumer complaint portal. Those tools exist precisely for the fee-and-consent problems that make these apps risky, and using them is how the pattern gets caught.

It can be reasonably safe if you use a token-based connection through an aggregator rather than sharing your raw bank password, and if you read the fee screens carefully. The bigger risk is usually undisclosed fees and tips, not theft.

Unauthorized electronic transfers are covered by the Electronic Fund Transfer Act and Regulation E, which give you dispute and error-resolution rights with your bank. If money leaves your account without authorization, that is your practical protection. Authorized debits you agreed to, including auto-repayment, are a separate matter.

Plaid is a data aggregator that connects apps to your bank. In a token-based connection you log in at your own bank and the app receives a revocable permission token rather than your password, which is generally safer than direct screen scraping. Aggregators have faced privacy litigation, so it is still worth checking what data is retained and shared.

Not always in the standardized way you might expect. The Truth in Lending Act would normally require cost disclosures, but as of December 2025 the CFPB's position is that qualifying EWA products are not credit under TILA, so those federal disclosures may not attach. State rules vary, which is why reading each app's terms matters.

In November 2024 the FTC brought an action against Dave, alleging undisclosed express fees, a default 15% tip many users thought was mandatory, and an undisclosed $1 monthly membership fee. The FTC referred the matter to the Department of Justice in December 2024. These are allegations, and the case was not a final judgment.

Cancel any subscription inside the app, then revoke the connection through the aggregator's portal (such as Plaid) and your bank's connected-apps settings. Deleting the app alone does not cancel a membership or cut off bank access.

See exactly how cash advance apps work, from linking your bank to the payday auto-debit, so nothing about them feels mysterious.

Read article

Earned wage access vs payday loans: how they compare on interest, repayment, and the protections that apply to each.

Read article

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking