June 23, 2026

Cash Advance Apps With High Limits, Ranked

Which cash advance apps offer the highest limits, how to qualify for more, and why the advertised max rarely matches your first advance.

Read article

An app tells you there is no interest and no mandatory fee, then hands you $100 before payday. It sounds like a favor. It is not a favor, because no company floats millions of people money out of kindness. The money has to come from somewhere, and the honest question is not "is this free" but "where, exactly, do they get paid, and how much of it comes from me." Once you can see the levers, you can price any advance in your head before you tap confirm.

Let me take the word "free" apart, then run a single realistic $100 advance through every charge so you can see the real total.

Earned wage access fees almost always come from one of three levers, and understanding them is the whole game:

Here is the pattern worth memorizing: an app that drops one lever usually leans harder on another. Kill the subscription and the express fee carries the model. Kill both and tips do the heavy lifting. Nobody in this business gives away all three.

Some apps charge a recurring membership. Brigit runs a monthly fee with a Plus tier and a higher Premium tier. Dave charges a small monthly membership (up to $5, per its own fee schedule) on top of a per-advance service fee. Others, including EarnIn, Klover, and MoneyLion's Instacash, carry no mandatory monthly fee at all.

A subscription is the easiest cost to reason about because it does not move. If you pay $9.99 a month and take four advances, the membership costs you about $2.50 per advance. If you take one, it cost you $9.99 for that one. The trap with subscriptions is not the amount, it is forgetting to cancel. A $9.99 membership you stopped using is $120 a year for nothing, which is worse than any express fee I can name.

This is the most important paragraph in the article, so I will be blunt. In its July 2024 study of the paycheck advance market, the CFPB found that expedited-delivery fees made up 96.6% of all consumer-paid fee revenue by dollar value in its employer-partnered sample. Ninety-six point six percent. The "free" version of nearly every app is the slow version, and most people, in the moment they need money, pay to skip the wait.

The same report pegged the average fee at roughly $3.18 per transaction, and found that 91.3% of workers paid at least one fee, averaging about $68.88 in fees per worker per year. So the typical user is not getting a free product. They are getting a product that costs them around $69 a year in small, easy-to-miss increments.

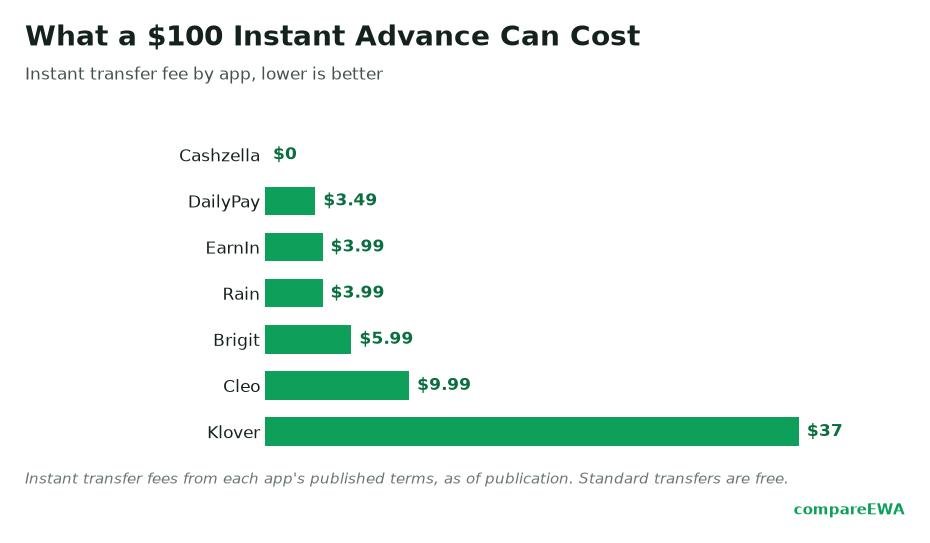

The dollar amount per advance sounds trivial. That is the point. A $3.99 charge to move $150 does not register as expensive. Take it 30 times a year, which is close to the industry average frequency, and you are near $120 in express fees alone.

Tips are the quietest lever, and the one regulators have gone after hardest.

On paper, a tip is a gift you choose to leave. In practice, the app often pre-selects a default tip, wraps it in feel-good language about keeping the service running, and makes zeroing it out a small act of guilt you have to perform under time pressure. In November 2024, the FTC took action against Dave, alleging the app charged undisclosed "Express Fees" of roughly $3 to $25 and steered users into "tips" of 10% to 20%, and that Dave reported more than $149 million in tip revenue from 2022 through the middle of 2024. That is not a rounding error, and it is not what most people picture when they hear the word "tip."

The District of Columbia went further with a separate suit against EarnIn, alleging that once tips and express fees were counted, the real cost of its "no mandatory fee" advances averaged an effective APR above 300%. That figure is an allegation from a state complaint, not a proven finding, so hold it as a claim rather than a verdict. But it points at the same truth: "optional" and "no mandatory fee" are marketing frames, not a promise that the advance was free.

Enough abstraction. Say you take a single $100 advance and want it instantly. Here is a realistic build-up of the cost, using figures in the ranges these apps actually charge:

Total real cost on that $100: roughly $9.50. You borrowed a hundred dollars for maybe a week and paid about nine-fifty for the privilege. On a subscription-free app with a $4 express fee and no tip, the same advance costs $4. On the free standard transfer with no tip, it costs nothing but arrives in a few days.

Notice what that spread tells you. The advance is identical. The cost swings from $0 to nearly $10 based entirely on choices you make at checkout, mostly the choice to go instant.

You will see people convert these fees into a jaw-dropping APR, and the math is real, so it is worth understanding rather than dismissing.

APR annualizes a cost. Take that $9.50 on a $100 advance repaid in one week. Stretch that same weekly rate across a full year and it annualizes into triple digits fast. The CFPB's 2024 analysis illustrated an average of roughly 109.5% APR, and about 580% on a small $50 advance, precisely because a flat few-dollar fee on a short repayment window looks enormous once you annualize it.

Two honest caveats here. First, you are not borrowing for a year. You repay in days, so the APR overstates what you actually hand over on any one advance, even as it correctly flags how expensive the habit is if you repeat it constantly. Second, that 109.5% and 580% framing came from a CFPB proposal that was later withdrawn. It is an illustrative estimate, not a required legal disclosure.

The rulebook shifted recently, and the current state matters because it explains why these costs are so easy to miss.

In December 2025, the CFPB issued an advisory opinion reaffirming that qualifying earned wage access is not "credit" under the Truth in Lending Act, and that optional expedite fees and tips are not finance charges. The practical result: these apps are not required to show you an APR the way a credit card or payday lender must. There is no standardized "here is what this costs" box mandated on the screen. That does not make the fees disappear. It means you are the one who has to add them up, because the law does not force the app to do it for you in a single comparable number.

So treat any older headline calling these products "secret 300% loans" as commentary from a moment when regulators were leaning the other way, not as a statement of current law. And treat the FTC's action against Dave for what it is: proof that the fine print, the tips, and the express charges are exactly where you should look before you trust the word "free."

Rarely, in practice. Many apps have no interest and no mandatory fee, but most users pay an express fee to get money instantly, and some leave a tip. The CFPB found the typical user paid around $68.88 a year in fees. The free path (a standard transfer, no tip) exists, but it is slower, and most people do not take it.

It is a per-advance charge, usually a few dollars, to receive your money in minutes instead of waiting one to three business days for a free standard transfer. Expedited-delivery fees are the industry's main source of consumer-paid revenue, making up 96.6% of it in the CFPB's employer-partnered sample.

No. Tips are optional, and you can set them to zero. The friction is that apps often pre-select a default tip and frame skipping it as withholding support. The FTC alleged Dave collected more than $149 million in such tips, so read the tip screen carefully and lower it to zero if you want to.

Because a small flat fee on a very short repayment window annualizes into a large percentage. A few dollars on a $100 advance repaid in a week looks like triple-digit APR once you stretch it across a year. The CFPB illustrated averages near 109.5%, though that framing came from a proposal it later withdrew, and these apps are not currently required to disclose an APR.

It depends on how often you take advances. If you take one advance a month, a $9.99 subscription can cost more than a single $4 express fee. If you take four instant advances a month, a subscription that waives express fees may work out cheaper. Add up your real usage before deciding.

It should not, but disclosure has been a real problem. The FTC's 2024 action against Dave centered on allegedly undisclosed express fees and non-consensual tips. Read the fee schedule and every checkout screen before you confirm, and check your bank statement after your first advance to see what actually came out.

Which cash advance apps offer the highest limits, how to qualify for more, and why the advertised max rarely matches your first advance.

Read article

A simple framework for choosing a cash advance app: line up limits, real cost, speed, and eligibility on the same criteria.

Read article

Instant cash advance apps promise money in minutes. See how fast they really are and what that speed costs per advance.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking