June 26, 2026

Earned Wage Access Fees: What They Really Cost

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

Most "best cash advance apps" articles hand you a ranked list and hope you trust it. The problem is that lists go stale the week fees change, and they never tell you why the number one pick is right for your situation instead of someone else's. A better approach is to learn a method: score every app you consider on the same handful of axes, and the winner for your paycheck sorts itself out. Do that once and you can size up an app this article never even mentions.

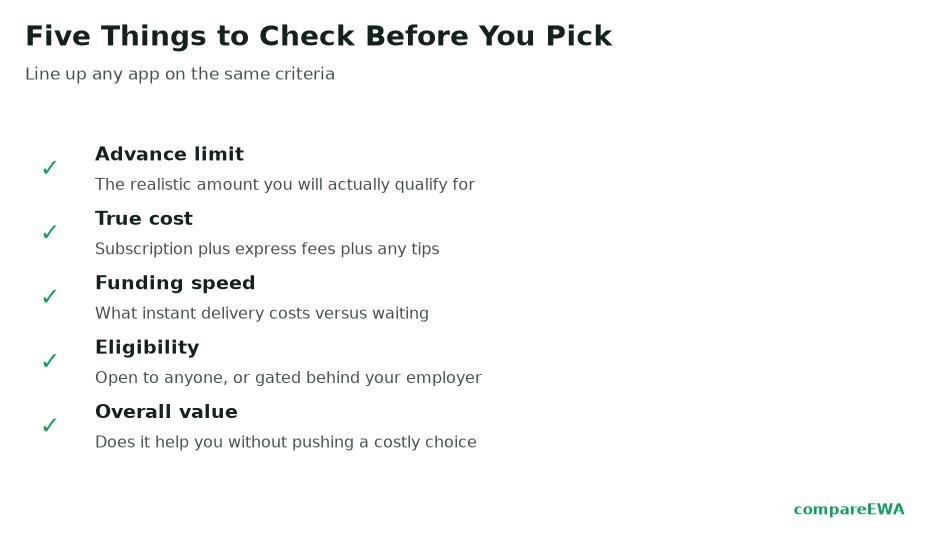

So instead of naming a champion, let me give you the five criteria I use to line any two apps up on identical terms, plus a worksheet you can run in about five minutes.

The apps in this category are more alike than the marketing suggests. They all advance a slice of money you have earned, they all offer a slow free transfer and a fast paid one, and they all pull repayment from your account on payday. What separates them is a set of tradeoffs that matter differently depending on how much you need, how fast, and how steady your income is.

That is exactly why a fixed ranking fails you. The cheapest app for someone who takes one advance a month is not the cheapest for someone who takes four. The app with the highest limit is useless if it is not offered in your state. A scoring method survives all of that, because you are grading each app against your circumstances, not against a reviewer's average user. Roughly 37% of U.S. adults could not cover a $400 emergency entirely with cash in 2024, according to the Federal Reserve's May 2025 report on household well-being, so plenty of people are choosing under real pressure. A method beats a guess when the stakes are your rent.

Start with the number, but the real one, not the billboard.

Advertised maximums of $500 to $1,000 are ceilings you climb toward, not what a new account gets. Most first-time limits land near $50 to $100 and grow as the app watches your deposits and repayments. So the question is not "what is the max," it is "what will this app realistically give me in the first month, and does that cover the bill in front of me."

Score it simply. If you need $80 and the app starts new users around $100, that is a strong match. If you need $400 now and the app starts at $100 with slow limit increases, it fails this criterion no matter how big its advertised ceiling is. Do not let a $1,000 headline distract you from a $100 reality.

This is the criterion people get wrong most often, because they compare headline prices instead of total cost.

Add up three things for the advance size you actually take: the subscription (amortized across how many advances you take a month), the express fee if you go instant, and any tip you would realistically leave. That sum is your real per-advance cost. And weight the express fee heavily, because the CFPB's July 2024 market study found expedited-delivery fees made up 96.6% of consumer-paid fee revenue. For most people, the instant-fee schedule matters more than the subscription price.

Run a quick example. App A has no subscription but charges $4.99 to move $150 instantly. App B charges $9.99 a month and waives express fees on its premium tier. If you take one instant advance a month, App A costs $4.99 and App B costs $9.99, so A wins. If you take four instant advances a month, App A costs about $20 and App B costs $9.99, so B wins. Same two apps, opposite answers, decided entirely by your frequency. The CFPB pegged the average user near 29.8 advances a year, so per-advance fees compound faster than people expect.

Speed is a paid upgrade on every app, so only pay for it when timing demands it.

The free standard transfer runs on ACH and takes one to three business days. The instant transfer lands in minutes for a fee. Here is the gut-check that saves people money: if your payday is four days out and the bill is due in three, the free transfer probably beats it there anyway. Paying $4 for instant in that situation buys you nothing but a few hours you did not need.

Score this against your real deadline, not your anxiety. Genuine same-day emergency, the rent-clears-tonight kind, justifies the express fee. A bill with a few days of runway usually does not. An app that makes standard transfers reasonably quick (say within a business day) scores higher than one where the free path drags to three days, because it widens the window where you can skip the fee.

An app you cannot use is a zero, no matter how good it looks.

Check the eligibility rules before you fall for the features: whether it requires direct deposit, how much regular income or account history it wants to see, and (for employer-linked apps) whether your workplace participates. Then check availability. State rules for earned wage access differ, and several states now register or license providers, so an app can be live in Texas and unavailable in your state. This is a moving target worth confirming on the app's own signup flow and against your state's specific EWA rules rather than assuming national coverage.

Score it as a gate, not a scale. If you are eligible and it operates in your state, it passes and you keep evaluating. If not, it is out, and you have saved yourself a wasted download.

This is the criterion competitor lists skip, and it is the one that can actually hurt you.

Every app auto-debits your repayment on payday. The questions that matter: When exactly does the pull happen, does the app let you reschedule if you will be short, and does it re-attempt a failed debit (which can stack a second overdraft on the first)? If an advance pulls $104 out of an account that only has $90, your bank may charge an overdraft fee around $35, which can dwarf the advance's own cost and defeat the whole point.

Score higher the apps that give you control: a clear repayment date, the option to delay, and some balance-protection feature that pauses the debit if your account is too low. Score lower the apps that pull rigidly on a fixed date with no flexibility. Frequent advances of about 30 a year, the industry average, mean this pull happens often, so a small design difference here adds up.

Before you commit, spend two minutes on the app's own fee page and its checkout screens. Can you find the express fee without hunting? Is the tip prompt honest, or is it a pre-filled default dressed up as generosity?

This is not paranoia. In November 2024 the FTC took action against Dave over allegedly undisclosed express fees and non-consensual tips, which is a real federal case built on exactly this problem. And because qualifying earned wage access is not regulated as credit as of the CFPB's December 2025 advisory opinion, these apps are not required to show you an APR, which means the burden of adding up the true cost falls on you. Consumer advocates like the National Consumer Law Center have argued that some "0% APR / earned wage" advances behave like high-cost payday loans once every fee is counted. That is an advocacy view rather than a regulator's finding, but it is a fair reason to distrust any "no interest" label until you have done the math yourself. An app that lays its costs out plainly earns trust points. One that buries them earns your suspicion.

Copy these six lines and fill them in for each app you are weighing. Give each a 1 to 5, except the eligibility gate, which is pass or fail.

Add up the five scored lines, drop any app that failed the eligibility gate, and the highest total is your best fit. Rerun it whenever fees change or your income does. The list-makers cannot follow your paycheck around. This worksheet can.

Total cost for how you will actually use it, not the headline. Add the subscription (spread across your monthly advances), the express fee if you go instant, and any tip, then compare that real number across apps. Because expedited fees are where most consumer money goes, the instant-fee schedule usually matters most.

No. A no-subscription app can cost more if you take several instant advances a month and pay an express fee every time. A subscription that waives or reduces express fees can beat it for frequent users. It depends entirely on your advance size and frequency, so run the math on your own usage.

Ignore the "no interest" label and total the actual fees: subscription, express charge, and tip, for the advance you would really take. Since these apps are not required to show an APR, you have to build the comparison yourself. The app with the lowest all-in cost for your usage wins.

Generally no. Most cash advance apps do not run a hard credit check and do not report advances to the major credit bureaus, so using one typically does not raise or lower your credit score. They evaluate your bank activity instead.

Favor apps that let you reschedule the payday debit and that pause the pull if your balance is too low, and only borrow an amount your next paycheck can comfortably absorb. Check that the app does not aggressively re-attempt failed debits, since a repeated pull can trigger a second overdraft.

Only if you actually need that much and can realistically qualify for it. Advertised maximums are ceilings you grow into, not first-time limits, and the biggest tiers often require opening the provider's own checking account. Match the app's realistic limit to your real need instead of chasing the largest number.

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

Which cash advance apps offer the highest limits, how to qualify for more, and why the advertised max rarely matches your first advance.

Read article

Instant cash advance apps promise money in minutes. See how fast they really are and what that speed costs per advance.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking