June 26, 2026

Earned Wage Access Fees: What They Really Cost

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

When the bill is bigger than a typical $100 advance can cover, a car repair, a rent gap, a deposit you did not see coming, the only question that matters is who will hand you the most money, fast. Fair. But the honest answer comes with a warning attached, and skipping the warning is how people end up disappointed at the sign-up screen. The advertised maximum is almost never what a new user gets. So this is two things at once: which apps have the highest ceilings, and how you actually reach a ceiling instead of the small starting limit most people get on day one.

Let me give you the ranking, then the mechanics behind it, so the numbers mean something.

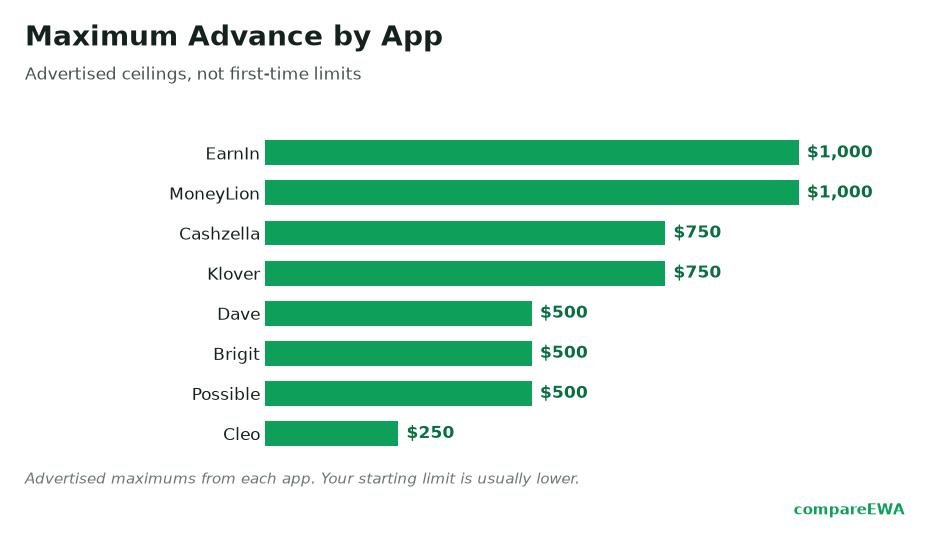

At the top of the range, a handful of apps advertise ceilings of $750 to $1,000, while a solid middle tier tops out around $500. Here is the lay of the land, with the figures each app or a major personal-finance publisher currently cites (verify on the app's own page before you commit, because these move):

So if raw ceiling is all you care about, EarnIn, Klover, Current, and MoneyLion's top tier lead, and Dave, Brigit, and Chime cluster at $500. But raw ceiling is not what you will get on Tuesday when you sign up, which is the part worth slowing down on.

Here is the gap nobody puts in the headline: many users start at $100 or less, no matter how big the advertised maximum is.

The reason is risk. When you are new, the app has almost no history with you. It does not know whether your income is steady, whether you will still be employed next month, or whether you will repay. So it starts small and low-risk, then raises the ceiling as you prove yourself. Dave is a clean example of how demanding the top of a range can be: reaching toward its ceiling effectively means showing regular deposits in the neighborhood of $1,000 or more a month. The "$500" on the billboard is real, but it is the reward for a track record, not the welcome gift.

Treat every advertised maximum as "up to," with an unstated condition attached. The question is never "what is the max." It is "what will this app actually approve me for in the first week or two, and does that cover my bill." If you need $400 today and the app starts new users at $100, its $750 ceiling does not help you today.

Account-linked apps read your checking-account history, often through an aggregator like Plaid, and look for a few specific signals. They generally want to see two to three consistent payroll deposits and roughly 60 to 90 days of account history before they get comfortable. Larger recurring deposits push your ceiling up. Steady, non-erratic spending helps. A balance that survives to payday reads as lower risk than one that hits zero every cycle.

To raise a limit, then, you feed the app the signals it wants:

None of this is fast. Limit-raising is a slow trust exercise, which is exactly why chasing the highest advertised ceiling is a poor strategy if you need a large amount right now.

The biggest numbers almost always come with the biggest strings, and MoneyLion is the textbook case.

MoneyLion's Instacash tops out around $500 for most users. The jump to $1,000 is not a matter of good behavior; it requires opening a RoarMoney checking account and moving your direct deposit into it. That is a real commitment. Rerouting your paycheck to a new account is a much heavier decision than taking a one-time advance, and it is the kind of thing you want to do because the account suits you, not just to reach a bigger advance you may use twice.

The pattern generalizes. When an app dangles its top tier, look immediately for the condition: an in-house checking account, direct-deposit rerouting, a premium subscription, or a long track record. The $1,000 is usually gated behind a change to your banking setup, and that trade deserves its own thought, separate from the urgency of the bill in front of you.

Two realities take some of the shine off a high limit.

First, cost scales with speed, not with generosity. A $500 ceiling means nothing good if getting that $500 instantly carries a steep express fee, and some apps scale their instant fee up with the advance amount, so the bigger the advance, the bigger the fee to rush it. A high limit and a high express fee often travel together. Price the instant transfer on the amount you would actually take before you celebrate the ceiling.

Second, and this is the one that bites, a bigger advance means a bigger repayment pulled on payday. Borrow $500 today and your next paycheck is $500-plus lighter when the auto-debit hits. If a $100 advance already leaves you leaning on the app each cycle, a $500 one leans harder, and it raises the odds of an overdraft if payday comes up short. The largest limit is not automatically the best choice. The best choice is the smallest advance that actually solves the problem, from an app whose real starting limit covers it and whose repayment your next check can absorb. That is a less exciting answer than "who gives the most," but it is the one that keeps you out of the loop where the advance becomes the problem.

Among the well-known apps, EarnIn advertises one of the highest ceilings at up to $750 to $1,000 per pay period for qualifying users, with Klover and Current up to $750 and MoneyLion up to $1,000 on its top tier. Most users start well below these maximums and grow into them over time.

Several advertise up to $500, including Dave ExtraCash, Brigit, and Chime MyPay, plus higher-ceiling apps like EarnIn and Klover. "Instantly" means paying an express fee for a fast transfer, and "up to $500" is a ceiling you qualify for over time, not a guaranteed first-time amount.

Yes, a few reach $1,000 per pay period, but with conditions. EarnIn cites up to $1,000 for some qualifying users, and MoneyLion offers up to $1,000 only after you open its RoarMoney checking account and route your direct deposit there. The $1,000 tier is not a first-time limit.

New accounts start low because the app has no history with you yet. Raise your limit by keeping direct deposits consistent, building 60 to 90 days of account history, repaying every advance on time, and linking additional income data where the app allows it. Limits rise gradually with a track record.

Usually, yes. Most apps want to see two to three consistent payroll deposits to verify your income, and larger regular deposits raise your ceiling. The highest tiers, like MoneyLion's $1,000, specifically require routing your direct deposit into the provider's own checking account.

It can. Some apps scale the instant-transfer fee up with the advance amount, so rushing a larger advance costs more than rushing a small one. A bigger advance also means a bigger repayment pulled on payday, which raises your overdraft risk if your paycheck comes up short.

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

A simple framework for choosing a cash advance app: line up limits, real cost, speed, and eligibility on the same criteria.

Read article

Instant cash advance apps promise money in minutes. See how fast they really are and what that speed costs per advance.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking