May 10, 2026

Does My Employer Offer Daily Pay? How to Check

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

Marisa works the floor at a distribution center for about $18 an hour. Last week the system gave her 38 hours. This week her Tuesday shift got cut when a shipment ran short, so she's looking at maybe 24. Her rent doesn't flex to match. She opened the earned wage access app her coworker swears by, and the number it offered her this week was a lot smaller than last week. She's not sure why, and she's a little worried that if she takes it, her Friday check is going to come up empty.

If that's you, this article answers the specific question the generic explainers skip: when your hours swing, how does an earned wage access (EWA) app decide what you're allowed to pull, and how do you avoid pulling so much that your actual payday deposit collapses? This applies to both flavors of EWA. Some of it comes through your employer's payroll, and some comes from a consumer app you sign up for on your own. The difference between those two matters a lot when your hours change, so I'll keep them separate throughout.

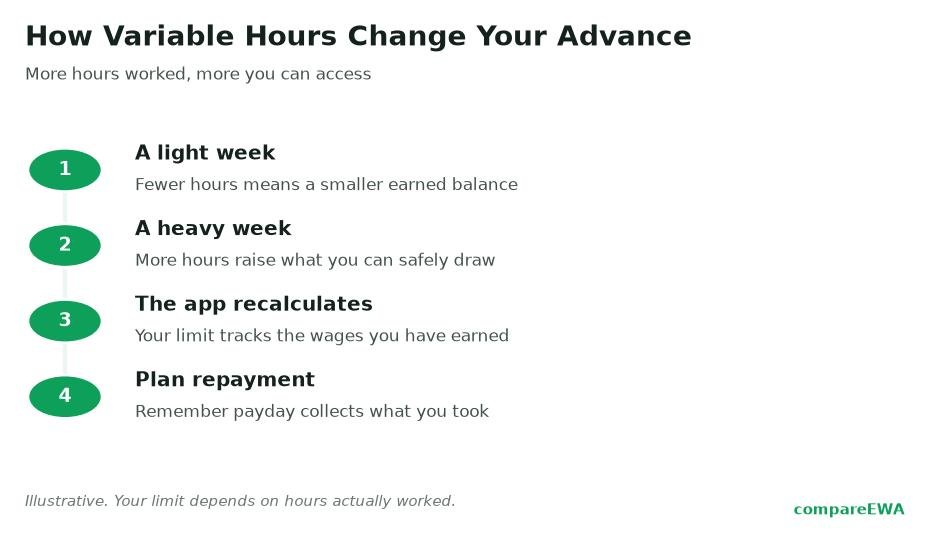

Short answer: yes. The catch is that a variable schedule directly changes the number you see, by design, and that surprises people.

Here's why. Earned wage access advances against wages you've already earned, not wages you're going to earn later. The available amount grows as you clock hours. So a 38-hour week builds up a bigger available balance than a 24-hour week, and a slow week shows you a smaller number. That's not the app being stingy or broken. It's the whole mechanism working exactly as intended: it can only offer you money you've actually worked for so far.

Once you understand that, the shrinking number stops feeling like a glitch and starts feeling like information. A small available balance is the app telling you this was a light week. That's worth knowing before you decide how much to pull.

The Congressional Research Service, in its July 2024 overview of earned wage access products, describes the core mechanic cleanly: these products let workers draw against accrued, verifiable earnings and then reconcile on payday, with the amount available depending on hours worked to date. Strip out the policy language and it means this. Every hour you work adds to a running total of earned wages. The app lets you access some slice of that total early. On payday, whatever you pulled gets subtracted from your check.

Notice the word "some slice." Almost no program lets you pull the entire amount you've earned. That limit is deliberate, and it's protecting you, which we'll come back to.

There are two ways an app can "know" what you earned, and the difference decides how well it handles variable hours.

Employer-provided or payroll-integrated EWA plugs straight into your employer's time-and-attendance and payroll system. It reads your verified hours. When you clock in and out, it knows. When Tuesday got cut, it knows that too. Because it's reading real data, it can track your earned wages precisely and adjust what it offers you in near real time.

Consumer sign-up apps are different. You download one on your own and link your bank account, and the app is not connected to your employer, so it can't see your hours at all. It estimates what you've probably earned from your history of bank deposits. Because it's guessing, it plays it safe. These apps commonly cap advances at a flat, conservative amount, often something like $100 to $250 to start, and raise it slowly as they see a pattern in your deposits.

This is the practical reason variable-hours workers often get lower, flatter limits from consumer apps. The app can't watch you accrue wages, so it hedges. An employer-integrated program, reading your actual clock-ins, can be more precise and often more generous because it isn't guessing in the dark.

Here's the part that catches people, and it catches variable-hours workers harder than anyone.

Whatever you pull mid-cycle comes out of the same paycheck. Pulling $120 on Wednesday is not extra money. It's $120 your Friday deposit is going to be missing. For someone on a steady 40-hour week, that's manageable; the check is predictable, so you know what's left. For someone whose hours swing, it's riskier, because you might pull a healthy amount during a good week and then get slammed with a slashed schedule the following week. Now your actual payday deposit, already thin from the short week, has your earlier pull carved out of it too. That's how a paycheck lands near zero.

The failure isn't the tool. It's pulling as if the good week will repeat, when the whole point of variable hours is that it won't. Take an advance sized to your best week and a bad week will punish you for it.

Most programs cap access at a percentage of what you've earned so far, not the full amount. Employer programs frequently limit access to somewhere around half of your net earned wages, though the exact percentage varies by provider and employer, so treat "roughly 50 percent" as a common pattern rather than a hard rule.

That cap is doing you a favor. If a program let you pull 100 percent of what you'd earned by Wednesday, you'd walk into payday with a $0 deposit and nothing to cover the weekend. Leaving a cushion behind is the point. So when the app won't let you take everything, it's not withholding your money. It's making sure Friday still has something in it.

Let's run Marisa's two weeks with round numbers so the mechanic is visible. She earns $18 an hour.

In the good week she works 38 hours. That's about $684 gross, and after taxes and deductions call her net earned wages roughly $540 for the period. Apply a 50 percent cap and she could access around $270 early. Say she pulls $120 midweek to cover a car repair. On payday, her deposit is what she earned minus that $120, so instead of the full net she sees about $420 land. Still a real check.

Now the slow week: 24 hours, about $432 gross, maybe $340 net. The 50 percent cap now offers her only about $170, less than half of what the good week offered, and that drop is the app honestly reflecting the short schedule. If she pulls $120 again out of habit, her payday deposit is only about $220. And if she'd pulled $120 in the good week and then hit this slow week, she's absorbing a light check on top of an earlier draw. Two pulls in two weeks, and payday barely exists.

The numbers make the rule obvious. The advance shrinks when your hours shrink for a reason. Match your pull to the week you're actually having, not the week you wish you were having.

When your hours bounce around, treat earned wage access as a bridge for a specific, unavoidable gap, not as a weekly supplement. Before you pull, ask what the money is for and whether Friday's check can survive without it. If you had a light week, pull less, or nothing. Keep a rough sense of what your next scheduled check looks like so you never carve into a paycheck that's already going to be short.

And if you find you're pulling every single week just to stay level, that's the signal that the timing gap has become a permanent shortfall, and no advance fixes a permanent shortfall. That's a budgeting problem to solve, not an app to lean on harder.

For scale, this is the majority experience, not a niche one. BLS reported that 80.3 million U.S. workers, 55.6 percent of all wage and salary workers, were paid hourly in 2024, and workers under 25 made up a fifth of hourly workers but 43 percent of those paid at or below the federal minimum. Another 4.47 million people worked part time in 2024 for economic reasons, meaning their hours were capped by circumstance, not choice. If your pay is never the same twice, you're in the biggest group in the American workforce, and these tools can work for you as long as you respect what the shrinking number is telling you.

Because earned wage access only lets you draw against wages you've already earned. Fewer hours means fewer earned wages, so the available amount is smaller by design. The lower number is the tool accurately reflecting a lighter week.

Yes. The available amount just scales with the hours you actually work, so it will be smaller than a full-timer's. Employer-integrated programs track your real hours; consumer apps estimate from your bank deposits and often start you with a low, flat limit.

Your advance is subtracted from that same pay period's deposit. If a big pull in a good week is followed by a short-hours week, your payday deposit can end up very small, so size any advance to the week you're actually having, not your best week.

It depends on the type. Employer-provided or payroll-integrated EWA reads verified hours straight from your employer's time system. A consumer app you sign up for on your own can't see your hours and estimates your available amount from your deposit history.

Often around half of your net earned wages, though the exact cap varies by provider and employer. The cap exists so a cushion remains in your paycheck and you don't end up with a $0 deposit on payday.

For variable hours, usually yes. Because it reads your verified hours instead of guessing, an employer-integrated program tracks your earnings more precisely and can offer more accurate, often higher limits than a consumer app that hedges with a flat, conservative cap.

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

How same-day and on-demand pay reshapes cash flow for workers used to a biweekly cycle, and the tradeoffs of pulling pay early.

Read article

How to manage irregular income when deposits arrive out of sync with your bills, using a simple week-by-week approach.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking