June 19, 2026

How to Stop Relying on Cash Advance Apps

A practical plan to treat cash advance apps as a bridge, not a habit, and shrink the advance you need each payday to zero.

Read article

If the word "budget" makes you tense up, you are not alone, and you are not the problem. Most budgets fail for boring, predictable reasons, and none of them are about you being lazy or bad at math. So instead of handing you one rigid system and telling you to white-knuckle it, I am going to walk you through a small menu of simple budgeting methods, each with the actual numbers worked out, so you can pick the one that fits how your brain and your paycheck really work.

Because that is the trick nobody says out loud: the best budgeting method is the one you will still be using in three months. Simple and repeatable beats perfect and abandoned. Every time.

Budgets usually collapse for one of three reasons. They are too detailed, so tracking every coffee feels like a second job and you quit by week two. They are too optimistic, built for the person you wish you were instead of the one buying groceries on Thursday. Or they are not matched to your pay rhythm, so a monthly plan falls apart when you actually get paid weekly and unevenly.

The fix for all three is the same: pick something low-maintenance, forgiving, and shaped like your real life. A budget that is 70% accurate and still running in June is worth infinitely more than a perfect spreadsheet you deleted in February. Keep that in mind as you read the methods below. You do not need all of them. You need one that sticks.

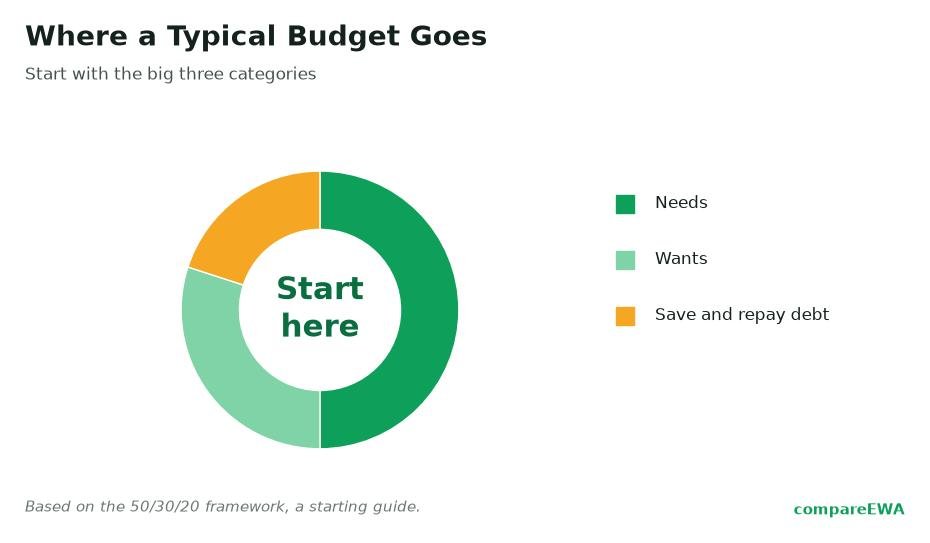

This is the famous one, popularized by Elizabeth Warren and Amelia Warren Tyagi in their book All Your Worth. The idea: split your take-home pay into 50% needs, 30% wants, and 20% savings or debt payoff.

Worked example: on a $2,000 monthly take-home, that is $1,000 for needs, $600 for wants, and $400 for savings and debt. Clean and easy to remember.

Now the honest part, because you have probably already spotted the flaw. On a tight income, needs routinely blow past 50%. Government spending data backs you up: the average U.S. household in 2023 spent 32.9% on housing, 17.0% on transportation, and 12.9% on food, which is about 63% on three needs alone before you have paid a single other bill. So if your "needs" are eating 70% of your pay, you are not doing it wrong. Treat 50/30/20 as a compass pointing in a direction (spend less than you earn, save something), not a rule you have failed if you cannot hit it exactly.

If tracking categories sounds exhausting, this one is for you. Pay yourself first means you automate a small savings transfer the moment your paycheck lands, before you spend a dollar. Whatever is left in checking is yours to spend freely, no logging required.

Worked example: your check hits, and an automatic transfer moves $40 into a separate savings account that same day. The remaining money in checking is your spending money, full stop. You do not track categories, you do not feel guilty about a purchase, because your saving already happened before you had the chance to skip it.

This works because it removes willpower from the equation. And it matters even in tiny amounts. Bankrate found that 27% of Americans had no emergency savings at all in its most recent reading, the highest share since 2020. A $40 automatic transfer that you never have to think about quietly puts you ahead of more than a quarter of the country.

If you actually like being in control of your money, zero-based budgeting will feel satisfying. The idea: assign every dollar of income to a category (bills, food, gas, savings, fun) until you have zero dollars left unassigned. Not zero dollars spent, zero dollars floating around without a purpose.

Worked example: you get a $1,500 paycheck. You assign $700 to rent, $150 to groceries, $80 to gas, $120 to utilities, $100 to your phone and internet, $50 to savings, $60 to fun, and so on, until the whole $1,500 has a job. Every dollar knows where it is going before the money is spent.

The strength here is that nothing slips through the cracks, because there are no cracks. The catch is that it needs a little upkeep each payday. If you are someone who finds that structure calming rather than annoying, this is probably your method.

Some categories are fine on their own and some quietly explode: groceries, gas, eating out, "fun." The envelope method caps exactly those. Traditionally people used literal cash envelopes; the digital version uses separate account balances or budgeting app categories that visibly block you when a category is spent out.

Worked example: you decide groceries get $100 a week. You load $100 into a grocery envelope (cash or a digital category). When it is gone, it is gone, and you eat from the pantry until next week. Because the limit is visible and physical-feeling, you feel the boundary before you overspend, not after the statement arrives.

You do not have to envelope your whole life. Just cap the two or three categories that tend to run away from you and let the rest breathe.

If you are paid weekly, biweekly, or irregularly, monthly budgeting can feel like guessing. So do not budget the month. Budget each paycheck as it arrives, against the bills due before the next one.

Worked example: you get paid every two weeks. When a $1,200 check lands, you look only at the bills due in the next 14 days: rent portion, one utility, groceries, gas. You assign this check to those, then set aside a slice for anything looming just past the window. When the next check comes, you do it again. You are always budgeting real money against near-term bills, never forecasting a whole month you cannot see yet.

This is the method most likely to survive irregular income, because it works with the money actually in front of you instead of an imaginary steady monthly total.

You do not have to buy anything to begin. Some of the best budgeting tools are free and come from sources with no product to sell you. The Consumer Financial Protection Bureau publishes free worksheets and a toolkit called "Your Money, Your Goals," and the FDIC offers a free financial-education curriculum called Money Smart. A plain notebook or a blank phone note works too. The method matters far more than the software. Anyone telling you that you need a paid subscription to budget is selling something.

Here is the shortcut. Match the method to your temperament and your pay:

You can also mix them. Plenty of people pay themselves first and cap groceries with an envelope. The only wrong choice is picking the most complicated one because it looks the most responsible, then quitting in two weeks. Pick the boring one you will keep.

Pay yourself first is usually the easiest to start, because it requires no daily tracking. You automate a small savings transfer on payday, and whatever stays in checking is yours to spend freely. It removes willpower and guilt from the process, which is why beginners tend to actually stick with it compared to detailed category tracking.

Not perfectly, and that is expected. On a tight income, needs often exceed 50% of take-home, since housing, transportation, and food alone average about 63% of household spending. Use 50/30/20 as a rough compass (spend less than you earn, save something) rather than a strict rule. Do not treat missing the exact ratios as a failure.

Budget each paycheck as it arrives instead of trying to plan a whole month. When a check lands, assign it to the bills due before your next paycheck, then set aside a bit for anything looming just past that window. This works with the real money in front of you, which is far more reliable than forecasting an uneven monthly total.

Zero-based budgeting assigns every dollar of income a job until nothing is unassigned, covering your entire budget. The envelope method caps specific categories that tend to overspend (like groceries or eating out) with a fixed balance that blocks you when it is gone. Zero-based is the whole plan; envelopes are a guardrail on your problem categories. Many people use both together.

No. Free options work just as well: the CFPB offers free worksheets and its "Your Money, Your Goals" toolkit, the FDIC has a free Money Smart curriculum, and a notebook or blank phone note costs nothing. The budgeting method matters much more than the software. You never need to buy a subscription to start.

Start with whatever amount you can automate and never miss, even $5 or $10 per paycheck. The habit matters more than the size early on. Since more than a quarter of Americans have no emergency savings at all, a small automatic transfer already puts you ahead. You can raise the amount later as you lower bills or income improves.

A practical plan to treat cash advance apps as a bridge, not a habit, and shrink the advance you need each payday to zero.

Read article

How to build an emergency fund on a low income, with realistic weekly amounts and habits that make a starter buffer stick.

Read article

Small, doable moves to make your paycheck last through the long last week before payday, built on realistic numbers.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking