June 8, 2026

How to Build an Emergency Fund on Low Income

How to build an emergency fund on a low income, with realistic weekly amounts and habits that make a starter buffer stick.

Read article

Every paycheck lands already spoken for. You know the feeling. The deposit hits, and before you have even looked at it, last week's advance takes its bite, and you are right back where you were, reaching for the app again. You keep telling yourself this is the last time. It has been the last time for a while now.

If that is you, take a breath. You are not weak or bad with money. You are caught in a loop that is designed to be sticky, and the way out is not willpower or going cold turkey (which usually ends in an overdraft anyway). The way out is a small, boring, repeatable method that shrinks the advance a little each pay period until you do not need it at all. Let me walk you through it.

First, the thing that will make you feel less alone: this pattern is documented, not imagined. The CFPB looked at paycheck advance users and found they took an average of about 27 advances per year. California's financial regulator, the DFPI, studied direct-to-consumer apps in the state and found users averaged around 36 advances a year, with some people hitting 100.

Those are two different groups measured different ways, so I would not stack the numbers on top of each other. But they point at the same truth: for a lot of people, an advance is not a rare rescue. It is a standing line item, every single cycle. If your usage looks like that, you are not an outlier. You are the norm the data describes.

The mechanics are simple, and once you see them you cannot unsee them. When you advance $100 this week, next week's paycheck shows up $100 shorter, plus whatever fee or tip you paid. That smaller paycheck does not stretch as far, so the same gap reopens, so you advance again to cover it.

The loop is tight and fast. The DFPI found the average advance was repaid in about 10 days, so there is barely a breath between paying one back and needing the next. And the advances themselves are small: roughly 80% fell between $40 and $100. That is actually good news. A small loop can be unwound with small moves. You do not need a windfall to break it. You need to shave it down a little at a time.

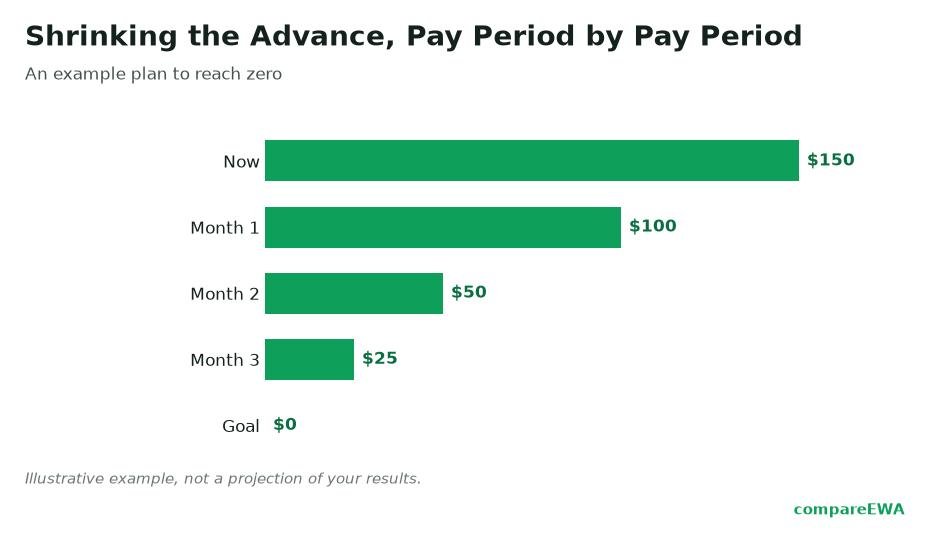

Here is the core method. Do not try to quit all at once. If you normally advance $120 and you suddenly advance $0, you will almost certainly overdraft, feel awful, and go right back to full-size advances. Instead, you step it down.

The step-down amounts here are just an example, not a magic formula. If $20 is too big a bite, use $10. If you can do $30 some months, great. The direction matters more than the speed.

Notice what the shrink-the-advance method is quietly building: a small cushion. That cushion is the whole point. The reason you reach for the app is a timing gap, and a buffer of even a few hundred dollars covers that exact gap without charging you a fee to do it.

You do not need a full emergency fund to get free of the app. You need enough to cover the shortfall the advance was covering. That might be $200, it might be $500, depending on your bills. The Federal Reserve's 2024 survey is a good reminder of why even a small buffer matters so much: only 63% of adults could cover a $400 emergency with cash, and 18% could handle less than $100 from savings. If you build a couple hundred dollars that most people around you do not have, you have already changed your position more than the numbers suggest.

While you climb out, plug the small holes that are quietly draining the cash you want to save. Three to check:

Every dollar you stop leaking here is a dollar that can go into the buffer instead, which speeds up the whole exit.

The advance is a symptom. The recurring shortfall is the cause. So while you shrink the advance, take one swing at the cause too, because sometimes a single change closes the gap entirely.

Pick one of these and actually do it this week:

You might have a rough week mid-plan and need cash. That is fine, and it does not undo your progress. Just try to reach for something cheaper than a full-price advance first. A small-dollar loan or line of credit at a credit union is often far cheaper than repeated express fees and tips. Asking a biller for a one-time extension costs nothing. And if your employer offers EWA through payroll, that version is frequently cheaper (sometimes free) than a consumer app, which makes it a better transitional bridge while your buffer fills in.

Let me put real numbers on it. Say you are paid every two weeks and you normally advance $120 each pay period, with a $5 express fee.

After eight weeks you have a $120 cushion, your advance is half what it was, and you are no longer paying a subscription or an express fee. Keep the same pace and within a few more cycles the buffer covers the whole gap, and the advance simply is not needed. That is the exit, built out of $20 steps you could actually manage.

Do not quit cold, which risks an overdraft. Instead, shrink the advance by a small fixed amount each pay period (for example $10 to $20) and move that same amount into a separate starter buffer. Over several cycles your paycheck catches up to your bills and the buffer covers the timing gap the app was covering, so you no longer need the advance.

Canceling the app itself will not hurt your credit, since most do not report to the bureaus. The overdraft risk comes from stopping advances too abruptly while your budget still depends on them. That is exactly why the step-down method exists: you reduce the advance gradually so your paycheck is never suddenly short.

Enough to cover the timing gap the app was covering, which is usually a few hundred dollars, not a full emergency fund. Since most advances fall between $40 and $100, a buffer of $200 to $500 is often plenty to break the reliance. Build it in small steps rather than waiting until you can save it all at once.

If you are advancing rarely, yes, because a flat monthly fee you pay whether or not you advance can cost more than the occasional advance is worth. Compare the monthly subscription to how often you actually use it. If the fee outweighs the benefit, cancel it and re-download later if you truly need to.

Free moves first: ask a biller to change a due date, request a one-time extension, or split a large bill into two paycheck-aligned payments. If you need cash, a small-dollar loan or line of credit at a credit union is usually cheaper than repeated express fees and tips, and employer-provided EWA through payroll is often cheaper than a consumer app.

It depends on how large your usual advance is and how much you can step down each cycle, but many people can meaningfully shrink or end their reliance within a few months by cutting $10 to $20 per pay period. The timeline is not fixed. What matters is steady movement in one direction, not speed.

How to build an emergency fund on a low income, with realistic weekly amounts and habits that make a starter buffer stick.

Read article

Small, doable moves to make your paycheck last through the long last week before payday, built on realistic numbers.

Read article

A step-by-step, shame-free plan to stop living paycheck to paycheck and build a little breathing room between deposits.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking