June 26, 2026

Earned Wage Access Fees: What They Really Cost

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

Skipping a monthly subscription feels like a clean win. No recurring charge, no membership draining $10 out of your account whether you use the app or not, just your advance when you need it. The instinct is right that subscriptions are worth avoiding. The catch is that "no monthly fee" does not mean "no cost." It usually means the cost moved somewhere else, and if you do not know where it went, you can end up paying more without a subscription than you would have paid with one.

So let me walk through the real no-subscription options, show where each one actually earns its money, and run the break-even math that fee-averse shoppers almost never see.

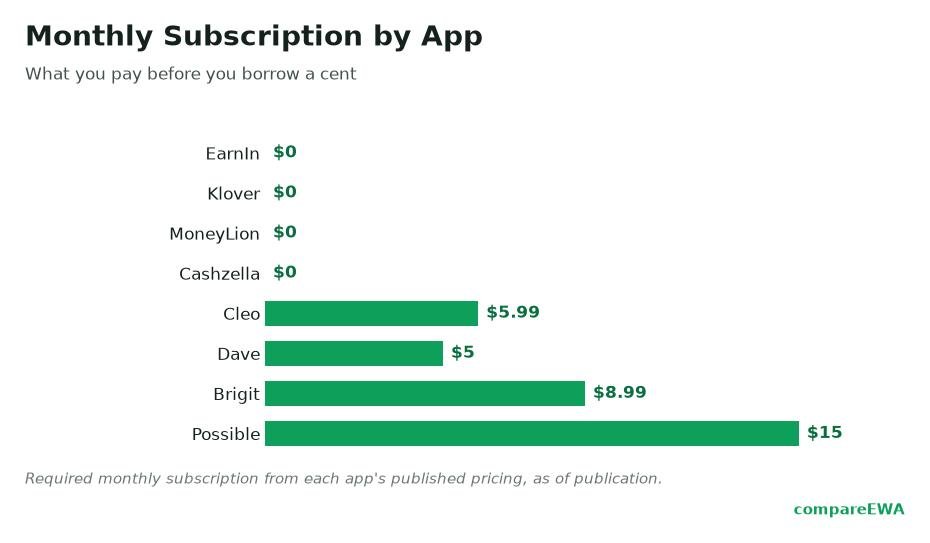

No monthly fee means one specific thing: there is no recurring membership charge. That is it. It does not mean there is no express fee to get your money fast, and it does not mean there is no tip prompt at checkout.

Think back to how these apps make money. There are three levers: the subscription, the instant-transfer fee, and the optional tip. Pull the subscription lever out and the company still needs revenue, so it leans on the other two. That is not a scam, it is just arithmetic. A business that advances millions of dollars has to be paid for the service somehow. The useful move is to stop asking "does it have a subscription" and start asking "if not, then how does it get paid, and how much of that lands on me."

Here are the common no-monthly-fee options, with the lever each one actually pulls:

Contrast those with the subscription crowd. Brigit charges a monthly membership. Dave charges a small monthly membership plus a per-advance service fee. The subscription apps front-load a predictable cost. The no-subscription apps back-load a per-use one. Neither is automatically cheaper.

Going no-subscription is not free, it is a set of tradeoffs. Three show up again and again.

Speed. The free path is the slow path on every one of these apps. No-subscription apps rarely give you fast money for nothing. If you want it in minutes, you are back to paying the express fee, which is the whole cost you were trying to avoid.

Limits. Some no-subscription apps start users at smaller amounts and raise the ceiling slowly. And the biggest limits often come with strings, like MoneyLion's higher tier that leans on opening a linked checking account. A missing subscription can quietly come with a smaller first advance.

Predictability. This is the sneaky one. A flat $9.99 membership is a known quantity. A per-advance express fee is not, because it scales with how often you tap the instant button. For a frequent user, unpredictable per-use fees can quietly total more than a flat membership would have.

Here is the comparison nobody runs, so let me run it. Treat this as a clearly hypothetical example with the assumptions stated, not a guaranteed result.

Assume you take four instant advances a month, and the no-subscription app charges a $4.99 express fee on each one. That is about $20 a month, or roughly $240 a year, in express fees. Now assume a subscription app charges $9.99 a month for a tier that waives or heavily reduces express fees. That is about $120 a year, membership included.

In that scenario, the "no monthly fee" app costs you roughly $240 a year and the subscription app costs about $120. The subscription is cheaper, by half, precisely because you were a heavy, instant-loving user and the per-advance fee punished the frequency. The CFPB's July 2024 market study found the average user takes about 29.8 advances a year, so plenty of people are in exactly this range, not the once-a-month range.

Flip the assumptions and the answer flips too. If you take one advance a month and use the free standard transfer, the no-subscription app costs you $0 a year while the subscription app costs $120. Now the no-fee app wins in a landslide. The lesson is not "subscriptions are good" or "subscriptions are bad." It is that your usage decides the winner, so you have to know your own pattern before you can pick.

When there is no subscription and the standard transfer is free, tips and express fees carry the entire business. That is worth saying plainly, because it reframes the "optional" language.

An "optional" tip that the app pre-selects, then presents under time pressure with a nudge about supporting the service, is optional the way a coat-check tip jar is optional. Technically yes, socially engineered to say yes. The FTC's November 2024 action against Dave centered on exactly this dynamic, alleging the app steered users into tips of 10% to 20% and reported more than $149 million in tip revenue over about two and a half years. Consumer advocates, including the National Consumer Law Center, have argued that some "0% APR" and "no mandatory fee" earned-wage advances behave like high-cost payday loans once every optional charge is counted. That is an advocacy position rather than a regulator's ruling, but it is a fair warning: a missing subscription is not the same as a free advance.

None of these apps is required to show you an APR, either, because the CFPB's December 2025 advisory opinion reaffirmed that qualifying earned wage access is not credit and that expedite fees and tips are not finance charges. That is exactly why per-advance costs slip past fee-averse shoppers. The one number that would make comparison easy is the number the law does not require them to print.

To be clear, no-monthly-fee apps are a good call for a lot of people. They are best for the light, patient user: someone who takes an advance occasionally, can wait one to three business days for the free standard transfer, and does not leave a tip. For that person, a no-subscription app can genuinely cost zero, and paying a membership would be lighting money on fire.

They are a worse fit for the heavy, instant user: someone who taps an advance several times a month and wants each one in minutes. That person pays the express fee over and over, and a fee-waiving subscription tier may actually be cheaper. If that is you, do not let "no monthly fee" talk you out of running the numbers. Skip a no-subscription app when your real behavior is frequent-and-instant, and reach for one when your behavior is occasional-and-patient. The label is not the decision. Your usage is.

Common no-monthly-fee options include EarnIn, MoneyLion Instacash, Klover (its Klover+ tier is optional), and Chime MyPay. None of them charge a mandatory recurring membership, though most charge a fee if you want your money instantly rather than in one to three business days.

Only if you use the free standard transfer and skip any tip. The subscription is just one of three cost levers. No-subscription apps still charge an express fee for instant funding and often prompt for a tip, so an instant advance on a "free" app usually is not free.

It depends on frequency. If you take several instant advances a month, a subscription that waives express fees can cost less than paying a per-advance fee every time. If you take one advance a month or use the free standard transfer, a no-subscription app is cheaper. Multiply your monthly express fees by twelve and compare that to an annual membership.

No. EarnIn has no mandatory fees and no monthly subscription. Its standard transfers are free and take one to two business days, while its instant "Lightning Speed" transfer costs a fee, and tips are optional.

Usually three things: speed (the free transfer is the slow one), sometimes a lower or slower-growing limit, and cost predictability (per-advance express fees scale with how often you use the app). For frequent instant users, those per-use fees can add up to more than a flat membership.

Sometimes. Some no-subscription apps start users at smaller amounts, and the largest limits often require extra steps, such as MoneyLion's higher tier tied to opening and routing direct deposit to its own checking account. Check the realistic first-time limit, not just the advertised maximum.

Earned wage access fees add up in quiet ways. See what a single $100 advance really costs once tips and instant fees are counted.

Read article

Which cash advance apps offer the highest limits, how to qualify for more, and why the advertised max rarely matches your first advance.

Read article

A simple framework for choosing a cash advance app: line up limits, real cost, speed, and eligibility on the same criteria.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking