May 10, 2026

Does My Employer Offer Daily Pay? How to Check

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

Ray drives four or five days a week and picks up warehouse shifts when the app is slow. Last week was strong, a couple of surge nights and a full Saturday, and his deposits looked great. This week the roads were dead and one warehouse shift got canceled, so his account is thin. Rent hit on the 1st either way. The frustrating part isn't that Ray doesn't make enough over a month. He does. It's that the money never seems to show up in the week the bills actually land.

If that's your life, whether you drive, nurse on call, work seasons, or earn on commission, this article is about one skill: smoothing uneven pay across a month so rent still gets covered the week your deposits are lean. Earned wage access and on-demand pay show up here, but as one tool in the kit, not the headline. This applies whether your early-pay option comes through an employer or a consumer app; I'll point out where that distinction changes things.

Let's name the thing precisely, because naming it points straight at the fix. Irregular-income stress is usually a timing mismatch, not a pure shortfall. The money arrives in lumps, and the bills arrive on a fixed calendar, and the two don't line up. You can earn plenty over four weeks and still hit a Thursday where the account is near empty and something's due Friday.

That reframe changes the whole approach. If the problem were "not enough money," the only answer would be earn more, which you may already be maxing out. But if the problem is timing, the answer is smoothing: catching money in the good weeks and releasing it evenly so the thin weeks don't crater. You're not trying to make more. You're trying to make what you already make show up when you need it.

This is common, and it's measurably hard. The Federal Reserve's 2024 household survey found 29 percent of adults had income that varied at least occasionally month to month, and it runs far higher for nontraditional workers: about 41 percent of gig workers and 59 percent of self-employed people reported month-to-month variation, versus 28 percent of people working for someone else. It's not just annoying, either. The same survey found 11 percent of adults struggled to pay their bills in the prior year specifically because their income varied, rising to 19 percent among people earning under $25,000.

Here's the core move, and it feels wrong the first time you do it. Build your budget around your lowest realistic month, or a conservative average of your recent months, not your best week.

Most people do the opposite without meaning to. A great week rolls in, the account looks healthy, and spending quietly rises to match. Then a slow week hits and there's nothing behind it. Budgeting off your low means your everyday spending is sized to survive a bad stretch. In the good weeks, you'll have a surplus, and that surplus has a job: it goes into a buffer. In the thin weeks, you draw from that buffer to pay yourself a steady amount. The lumps go in, a smooth paycheck comes out.

That's the whole method. Overpay your buffer when times are good, lean on it when they're not, and keep your baseline spending set to the floor rather than the ceiling.

The cleanest way to make smoothing actually happen is to split it across two accounts, because willpower alone rarely survives a flush week.

Set up a "hold" account where every irregular deposit lands. Don't spend directly from it. Then, on a fixed schedule, say every Friday, move a set amount, your self-paid "paycheck," into a separate "spend" account that your bills and daily life run from. You pick the paycheck number based on your worst-week budget, so it's sustainable even in a slow stretch. The hold account swells in good weeks and cushions the bad ones, while your spend account sees the same steady figure regardless of how wild the underlying income was.

It's a simple bit of plumbing, but it does something your brain can't do reliably on its own: it turns lumpy income into a predictable check. You stop reacting to every deposit and start living on a number you chose.

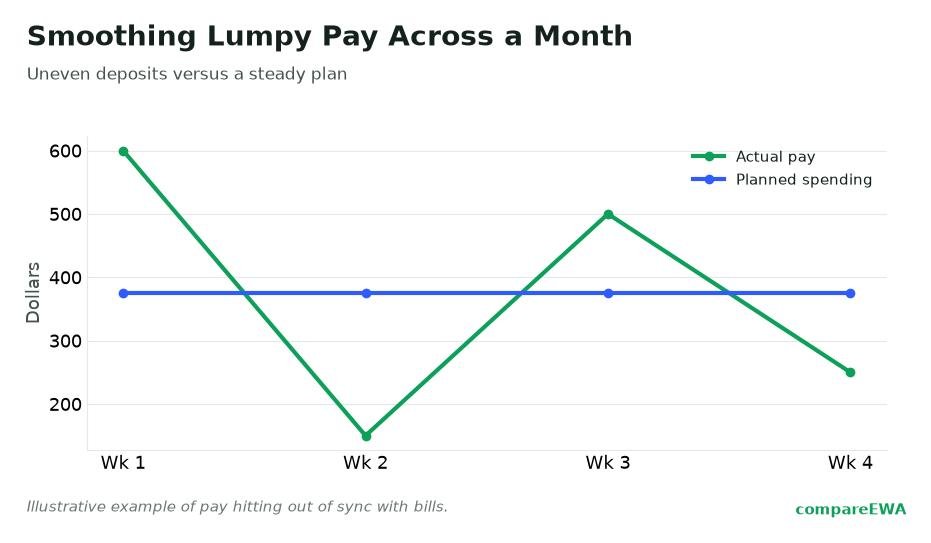

Let me walk one month so the mechanic is concrete. Say Ray needs about $2,800 a month to cover rent, utilities, phone, groceries, and gas, so his self-paid paycheck is $700 a week. His deposits land like this:

Notice that Ray's month had a great week and a near-disaster week, and his actual spending never wobbled. Every week he lived on $700. The buffer absorbed the shock. That's smoothing doing its job. Add the four deposits and he brought in $3,300 that month, comfortably above his $2,800 need, but that surplus only helped because the system caught it instead of letting it evaporate in week one.

Even with a buffer, sometimes a slow stretch outruns your cushion, especially early on before you've built one. When money truly won't cover everything, pay in this order.

This order matters because the emergency cushion that would normally absorb a bad week is thin for a lot of households. The Federal Reserve found 37 percent of adults in 2024 could not cover an unexpected $400 expense entirely with cash or its equivalent. If you're in that group, triage isn't failure, it's the correct response to a real constraint.

Now the honest place for earned wage access in all this. If you're a W-2 hourly or shift worker with access to EWA, whether through your employer or a consumer app, it can bridge a genuine timing gap in a thin week. Bill's due Thursday, payday's Friday, you pull a little to close 24 hours. Used that way, for a specific gap, it's a legitimate tool.

But be clear about what it is. Earned wage access borrows from the same paycheck, so it's a bridge, not a buffer. The buffer you built in your hold account is your money, sitting in reserve. An advance is next week's money, pulled forward. If you lean on it every single week, you're not smoothing anything, you're just moving the shortfall forward one deposit at a time, and eventually the checks you're borrowing against are all pre-spent. The Financial Health Network's 2023 EWA Users Report found people mostly use accessed pay for regular, recurring expenses like rent, bills, and fuel, not one-off emergencies, which is exactly why a smoothing system beats repeated advances: recurring costs need a durable fix, not a weekly patch.

So use early pay to cover a gap while you build the buffer. Once the buffer exists, you'll reach for the advance less, which is the point. The goal isn't to master borrowing from yourself. It's to not need to.

Budget off your lowest realistic month, not your best week. Pay yourself a steady weekly amount from a separate "hold" account where deposits land, banking the surplus from good weeks so you can cover the thin ones. Your spending stays flat even when your income swings.

Aim first for enough to cover the gap between a bad week and your steady self-paid paycheck, then build toward one month of core expenses. Even a small cushion changes a slow week from a crisis into a non-event, and the Federal Reserve found 37 percent of adults can't cover a surprise $400 expense with cash, so any buffer puts you ahead.

Use it to bridge a specific timing gap in a thin week, not as a weekly habit. It borrows from your next paycheck, so it's a bridge, not a buffer. Leaning on it every week just moves the shortfall forward instead of fixing it.

Housing and utilities first, then food, then obligations with grace periods. Call any biller you expect to be late with before the due date, since many will work out an arrangement if you reach out early.

Save in the good weeks, not the average week. When a strong deposit lands, move the surplus above your steady paycheck into the buffer before it gets spent. Automating that transfer keeps a flush week from quietly disappearing.

Budgeting off your lowest realistic month is safer, because a conservative average can still leave you short in a genuinely bad stretch. Set your baseline low, and treat anything above it as buffer fuel rather than spending money.

Does my employer offer daily pay? How to find out whether on-demand pay is available at work, who to ask, and what to expect.

Read article

How same-day and on-demand pay reshapes cash flow for workers used to a biweekly cycle, and the tradeoffs of pulling pay early.

Read article

How earned wage access works for hourly and shift workers with variable hours, and what you can safely pull before payday.

Read articleSee how the top earned wage access apps stack up on fees, limits, and speed. View the full ranking